Contents:

- Black and white lists of the Federal Tax Service: key aspects

- Updates to the black list of the Federal Tax Service: changes from 2025

- The impact of the black list of the Federal Tax Service on international companies and offshore companies

- Changes in the white list of the Federal Tax Service: key facts for 2025

- The impact of the white list of countries on the use of foreign bank accounts for residents of the Russian Federation

- The impact of changes in the lists of the Federal Tax Service on controlled foreign companies (CFC): real-world experience

- Recommendations for minimizing risks and fines in management Offshore accounts and CFCs in 2025

Starting a Business: 7 Steps from Idea to Implementation

Learn MoreFTS Black and White Lists: Key Aspects

The FTS black and white lists are key instruments for tax and currency control in Russia. These lists, which include countries and territories, play an important role for tax residents and their financial transactions. The black list contains states that do not comply with international tax standards, which may lead to increased attention from tax authorities. At the same time, the white list includes countries considered reliable partners for business and financial transactions. Understanding these lists helps tax residents avoid risks and ensure the legality of their financial transactions. The blacklist includes jurisdictions that fail to provide the Federal Tax Service with the necessary information on tax residents of the Russian Federation. This may be due to a lack of proper cooperation or unfair tax practices. In contrast, the whitelist includes countries with which automatic exchange of financial data has been established, significantly simplifying the tax administration process and promoting greater transparency in international financial relations. Having a whitelist helps attract foreign investment and improve a country's reputation internationally. The blacklist and whitelist are compiled based on an analysis of the state of information exchange between Russia and other countries. These lists are reviewed annually to ensure the information is up-to-date and reflect changes in international practice. This approach allows us to effectively respond to new challenges and improve the quality of data exchange, which is important for ensuring security and developing international relations. Individuals who control controlled foreign companies (CFCs), as well as holders of foreign bank accounts, should closely monitor changes in the relevant lists. A country's status on the black or white list can significantly impact taxation, reporting, and the ability to use offshore accounts. These changes can have significant implications for financial planning and compliance. I will discuss these aspects in more detail below. A controlled foreign company (CFC) is an organization registered outside of Russia that is controlled by Russian tax residents. It is important to understand the obligations and requirements imposed by Russian law on persons controlling CFCs. For more detailed information on this, I recommend checking out my previous publications, where I discuss in detail all aspects related to CFCs, including tax obligations and reporting rules.

Updates to the Federal Tax Service blacklist: changes from 2025

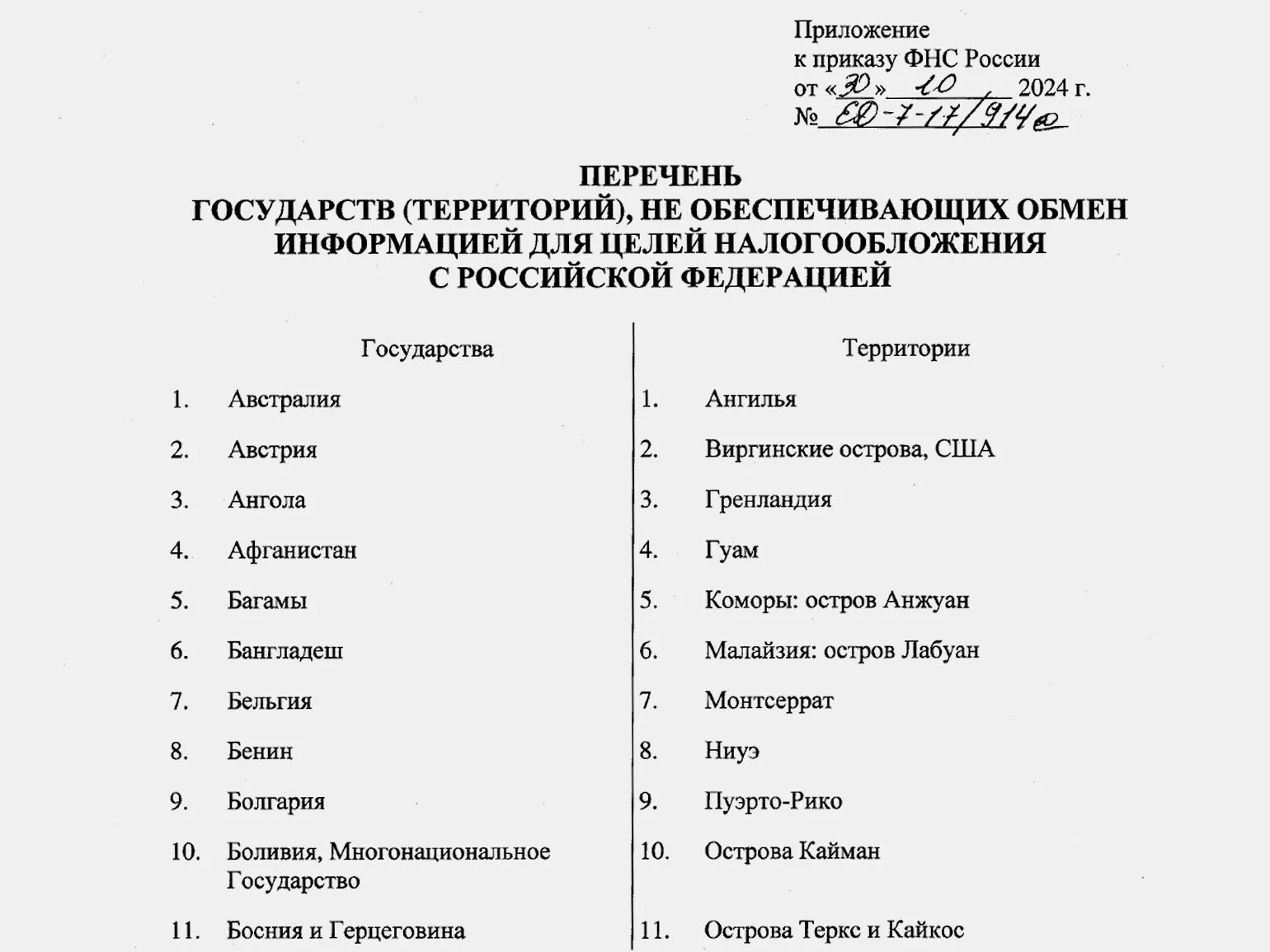

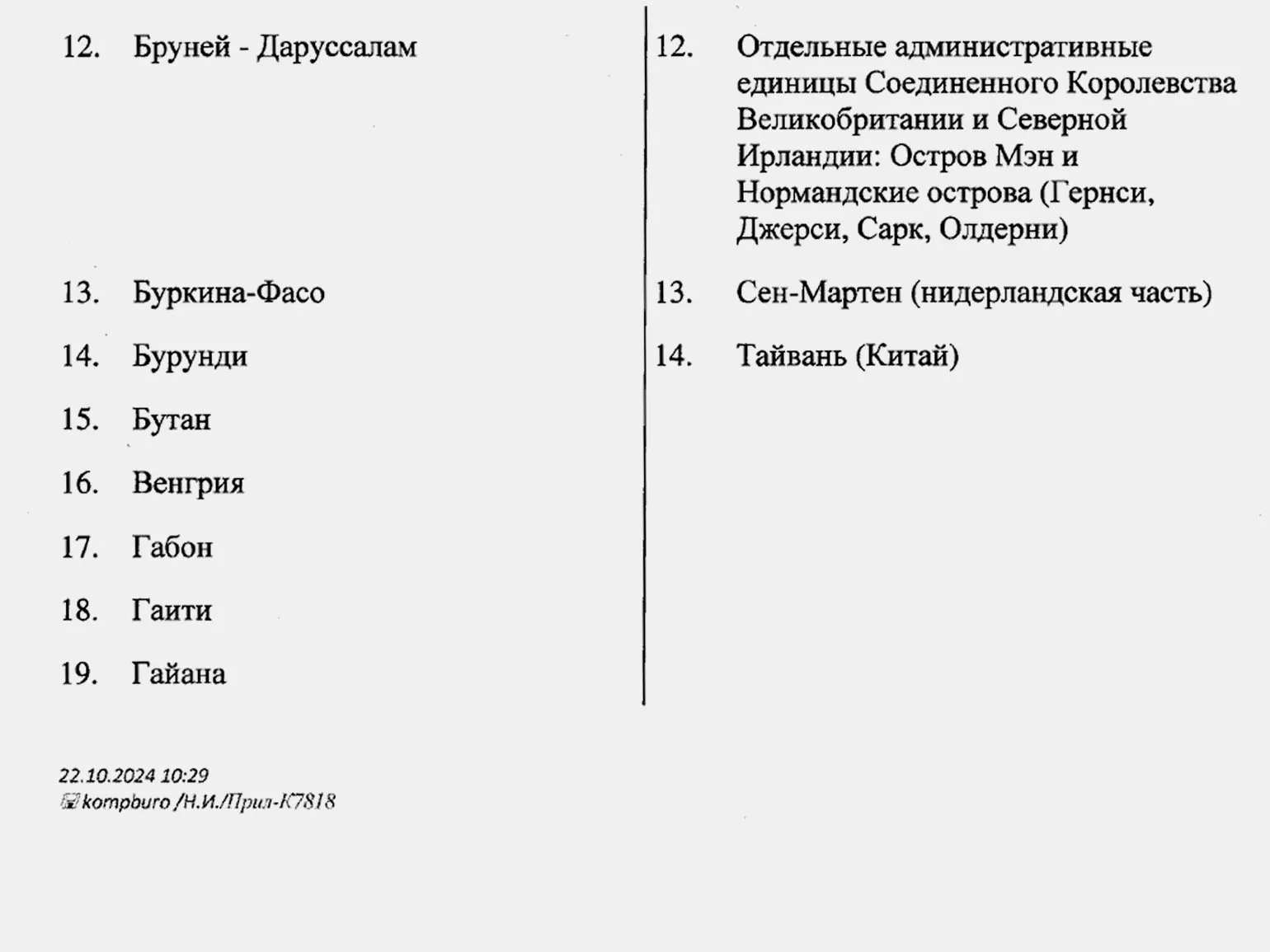

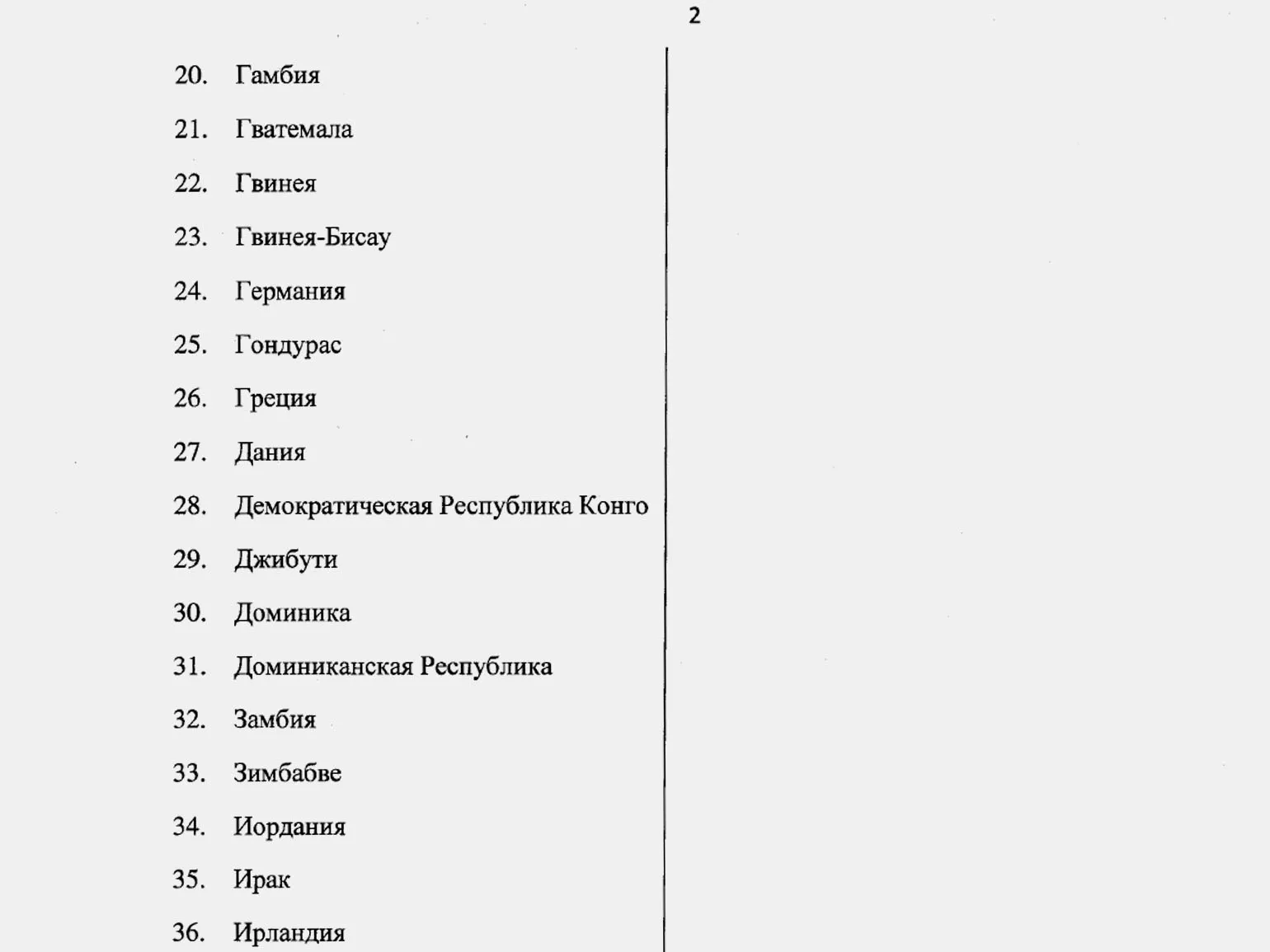

On December 31, 2024, Federal Tax Service Order No. ED-7-17/914@ dated October 30, 2024, came into force, introducing significant changes to the blacklist of countries. This update covers not only traditional offshore zones but also countries with developed economies, which highlights the efforts of the Russian authorities to combat tax evasion and increase the transparency of financial transactions. These changes may impact business structures and investment strategies, requiring companies to reconsider their tax obligations and approaches to conducting international business. It is important to keep information up-to-date and adapt your strategies to new legal requirements.

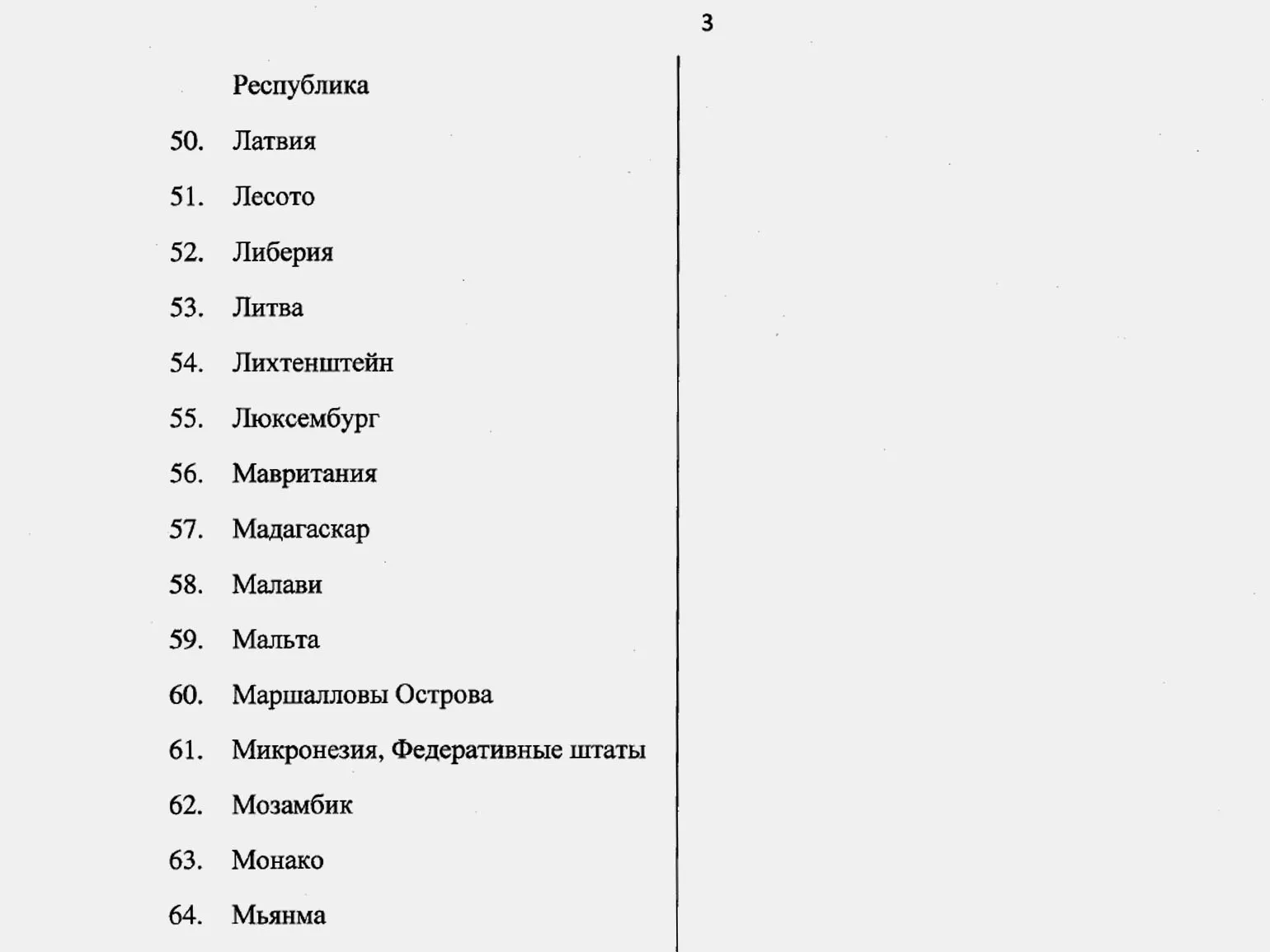

The updated blacklist includes all European Union countries, as well as Australia, Monaco, Liechtenstein, and New Zealand. These changes are due to the fact that these countries have limited or completely stopped the exchange of financial information with Russia. These measures could have a significant impact on financial transactions and international relations, highlighting the importance of transparency in financial interactions between countries.

Russian tax authorities face a serious problem due to the inability to obtain data on taxpayers registered in certain jurisdictions. This creates the risk of increased tax evasion and complicates the tax audit process. With a lack of information about the tax obligations of individuals and companies operating in such regions, the effectiveness of tax audits is significantly reduced. These circumstances may negatively impact the state budget and necessitate the development of new strategies for monitoring tax revenues.

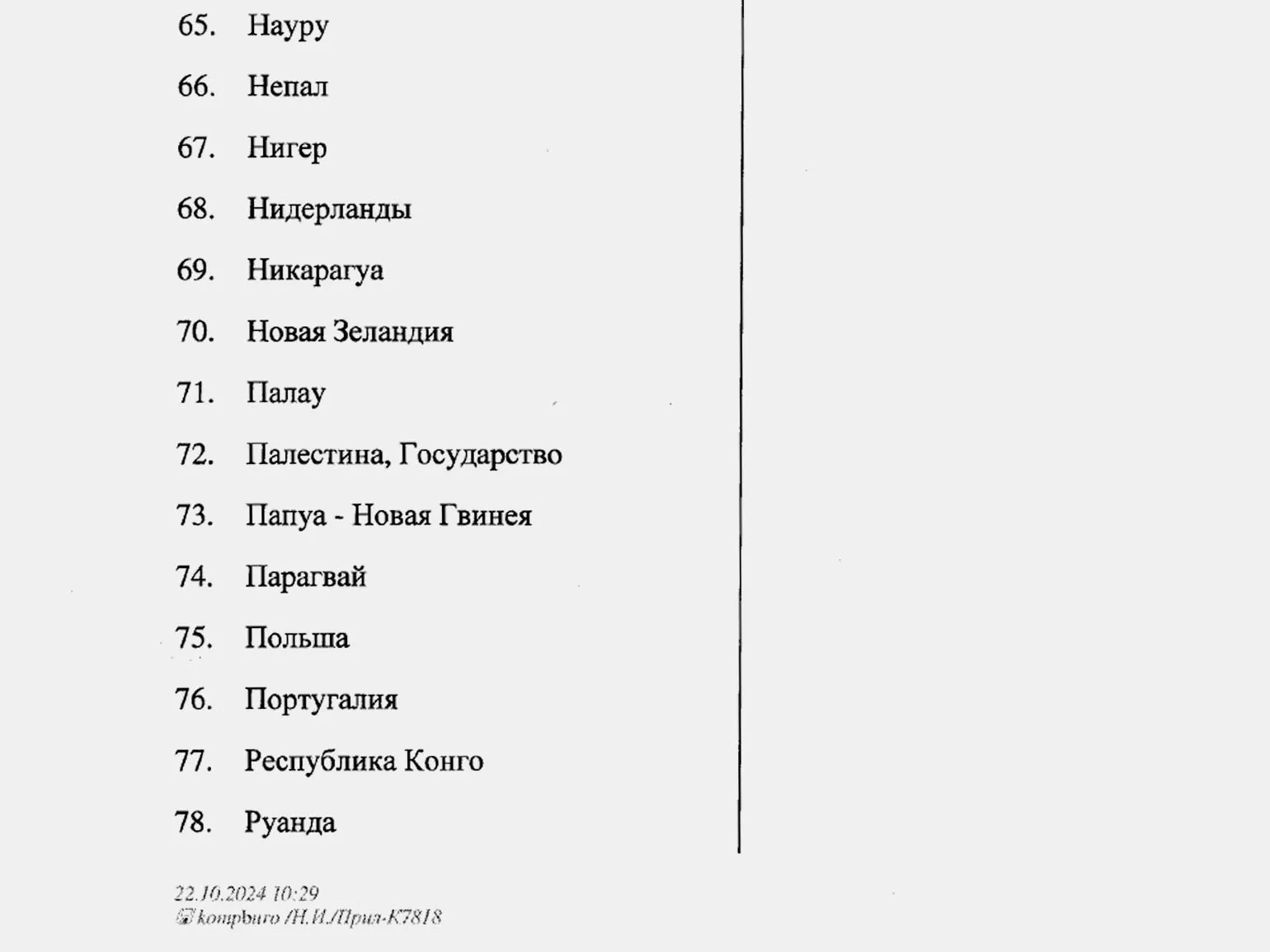

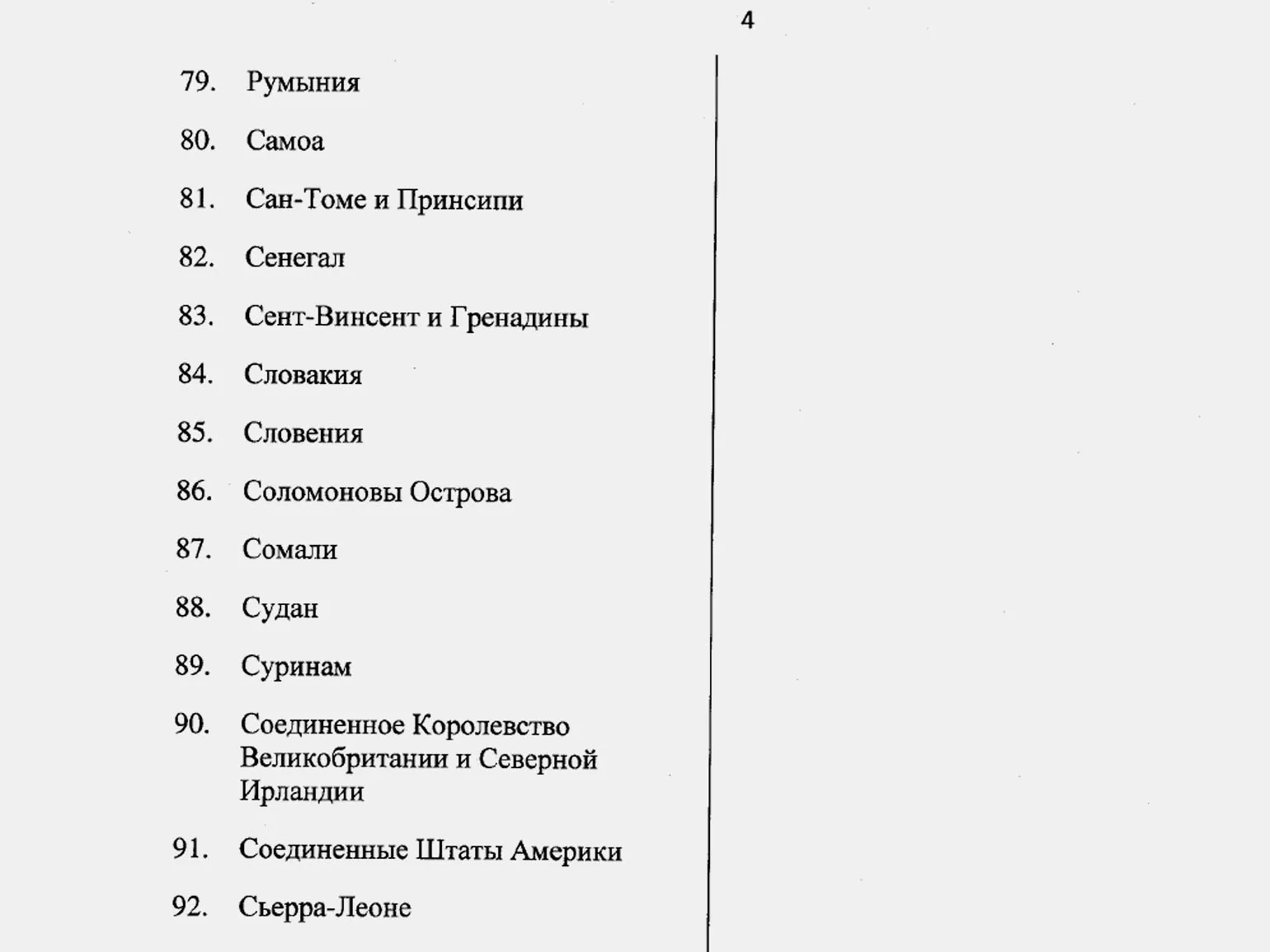

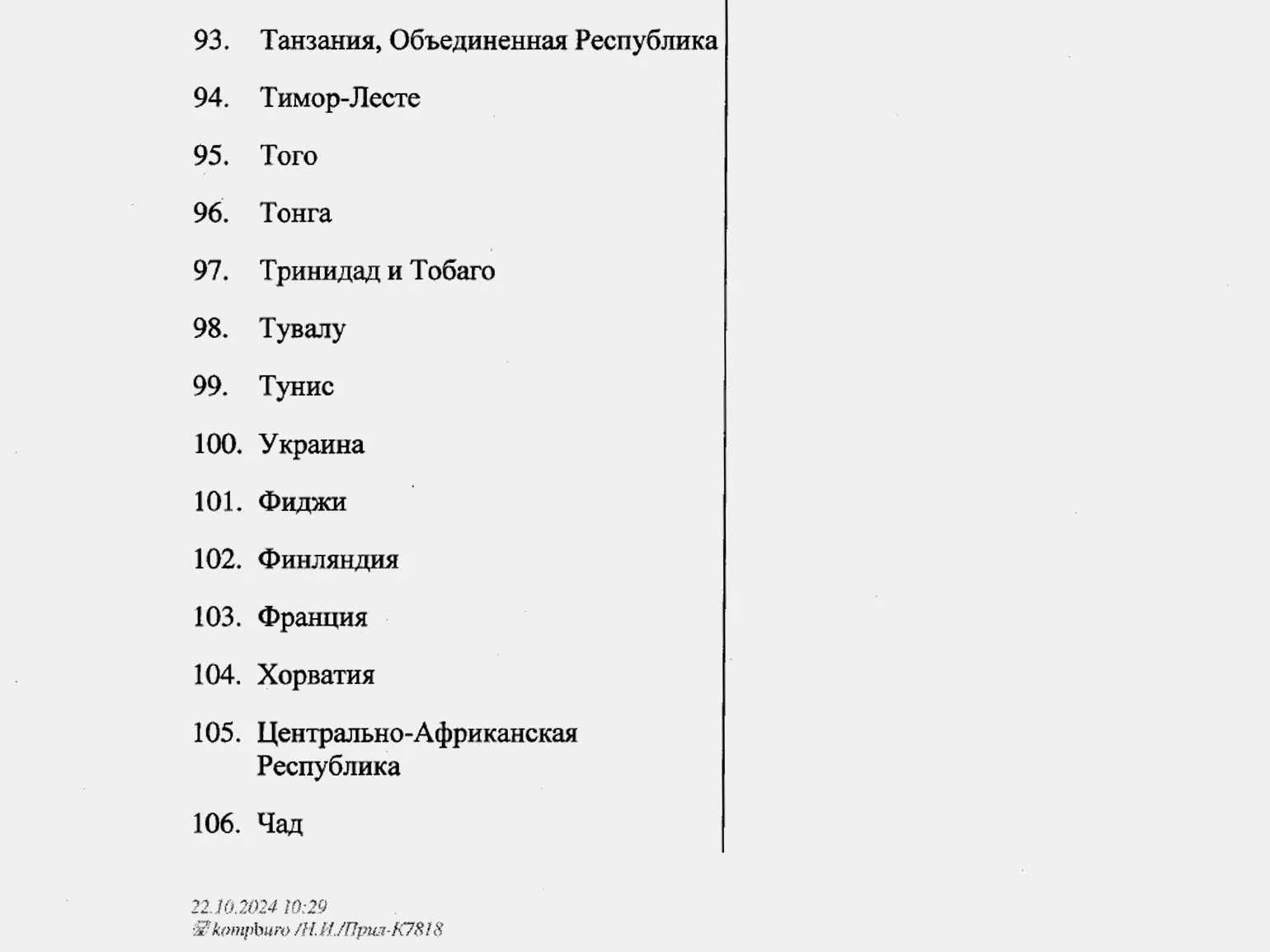

A full list of countries and territories that do not provide tax information to the Russian Federation can be found in the appendix to the order. This information is of significant importance for businesses interacting with foreign partners, as it helps optimize tax risks and ensures transparency in financial transactions.

Despite existing bilateral and multilateral cooperation agreements, they do not serve as grounds for removing countries from the blacklist. The Federal Tax Service (FTS) makes decisions based on the actual results of information exchange. This means that even the existence of agreements does not guarantee automatic deregistration. The effectiveness of interaction and the actual fulfillment of data exchange obligations remain key factors in assessing countries.

The Impact of the Federal Tax Service Blacklist on International Companies and Offshores

The inclusion of a country on the blacklist of the Federal Tax Service (FTS) of Russia creates serious difficulties for tax planning for controlled foreign companies (CFCs) registered in these jurisdictions. This decision significantly complicates business operations, as companies face increased tax risks and restrictions on financial transactions. As a result of this change, CFCs may lose access to low tax rates and face additional reporting and increased disclosure requirements. It is important to consider that such measures may lead to an increased tax burden and changes in investment strategies. Therefore, companies operating on blacklists need to carefully review their business processes and tax strategies to ensure compliance with the new requirements and minimize financial risks.

Limiting tax benefits for controlled foreign companies (CFCs) registered in blacklisted countries precludes the possibility of applying the tax benefits provided by the Tax Code of the Russian Federation. This primarily concerns exemption from profit tax, which negatively impacts the financial performance of these companies. Given these restrictions, it is important to carefully analyze the jurisdictions in which CFCs are registered to avoid losses associated with tax liabilities.

An auditor's report is a mandatory document for submitting financial statements to the Federal Tax Service of Russia. Companies on the blacklist of controlled foreign companies (CFCs) must include an auditor's report in their reporting documents. The absence of such a report makes it impossible to confirm the amount of profit, even if the financial statements are prepared in accordance with the laws of the country of registration. Therefore, it is important to ensure a high-quality audit report to ensure tax compliance and avoid penalties.

The risk of double taxation arises when a blacklisted controlled foreign company (CFC) receives dividends from a Russian company and then transfers them to a Russian individual, for example, a CFC owner. In such a situation, the individual is unable to reduce the amount of personal income tax (PIT) by the amount of profit tax withheld in Russia. This leads to an increase in the overall tax burden and a decrease in the financial attractiveness of such transactions. Therefore, it is important to consider the risks associated with double taxation when planning a tax strategy and choosing an asset ownership structure.

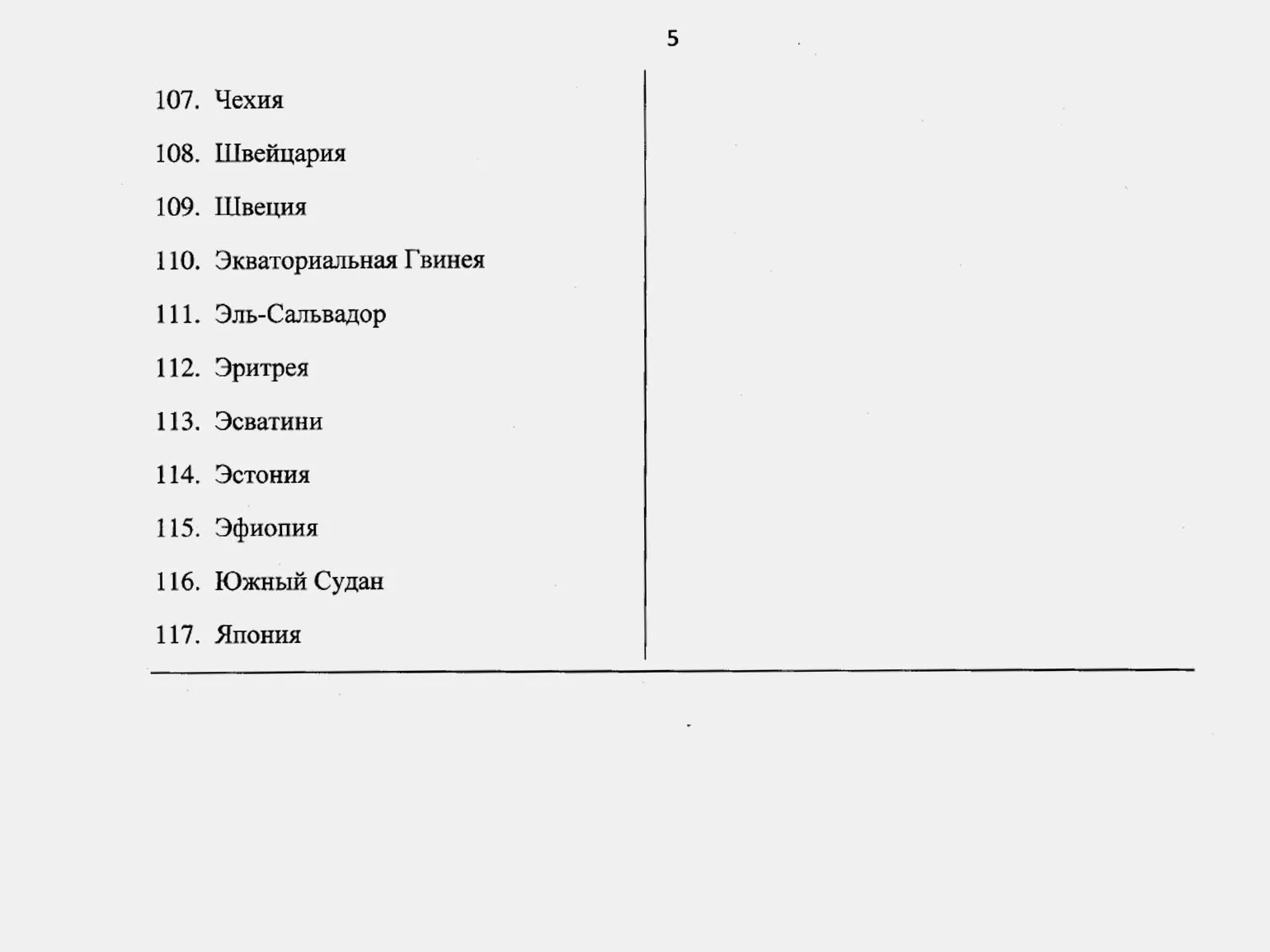

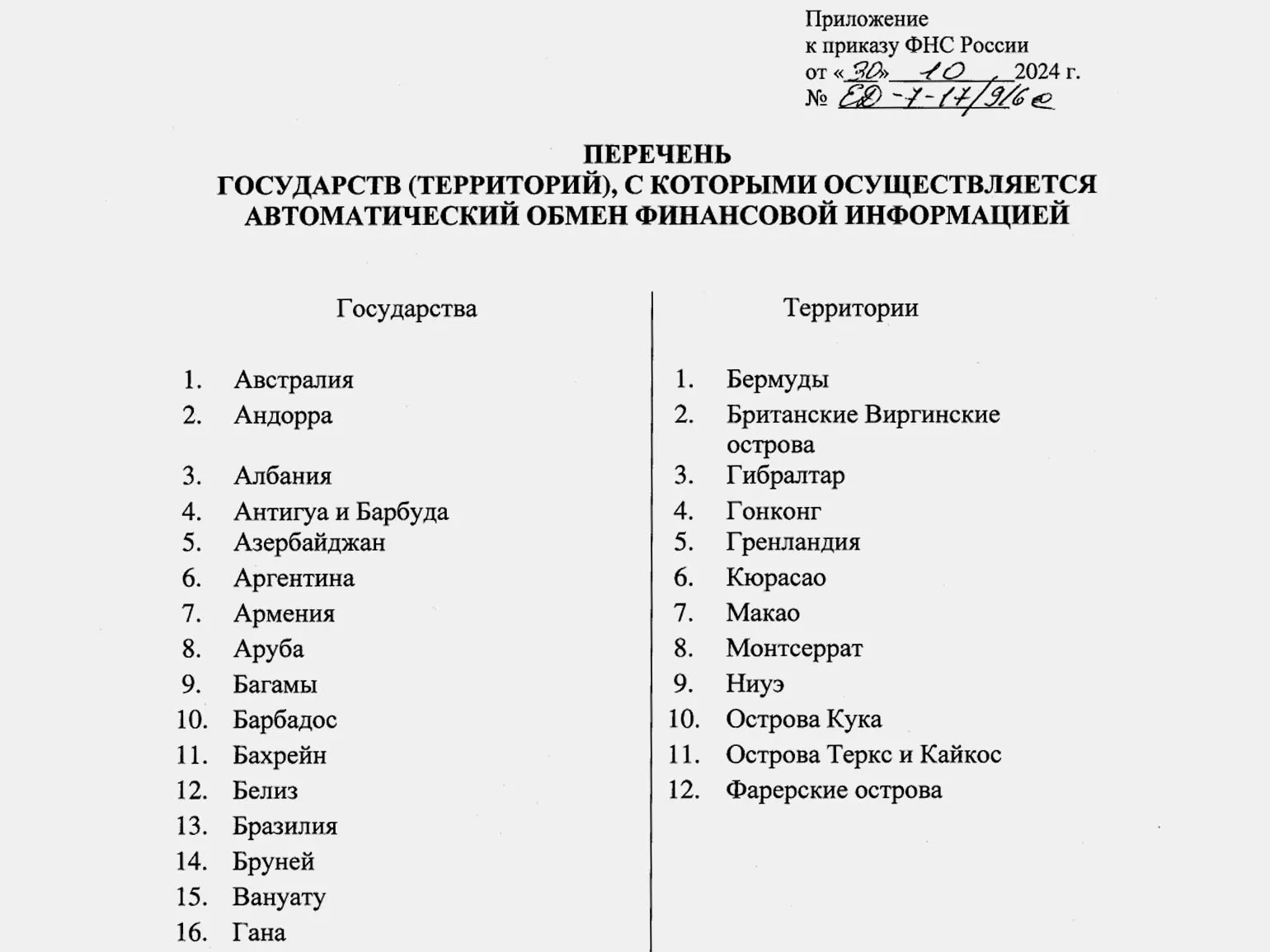

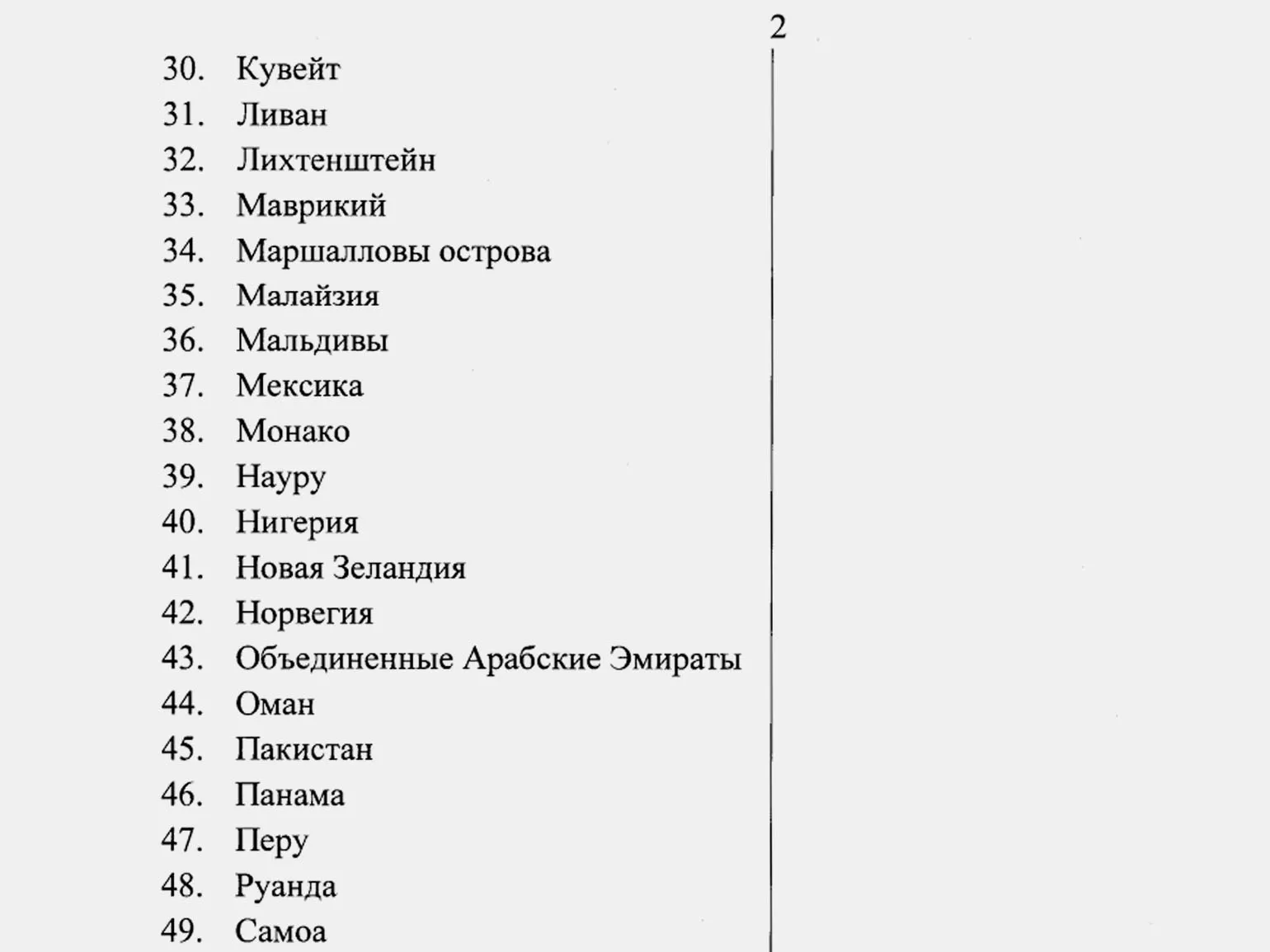

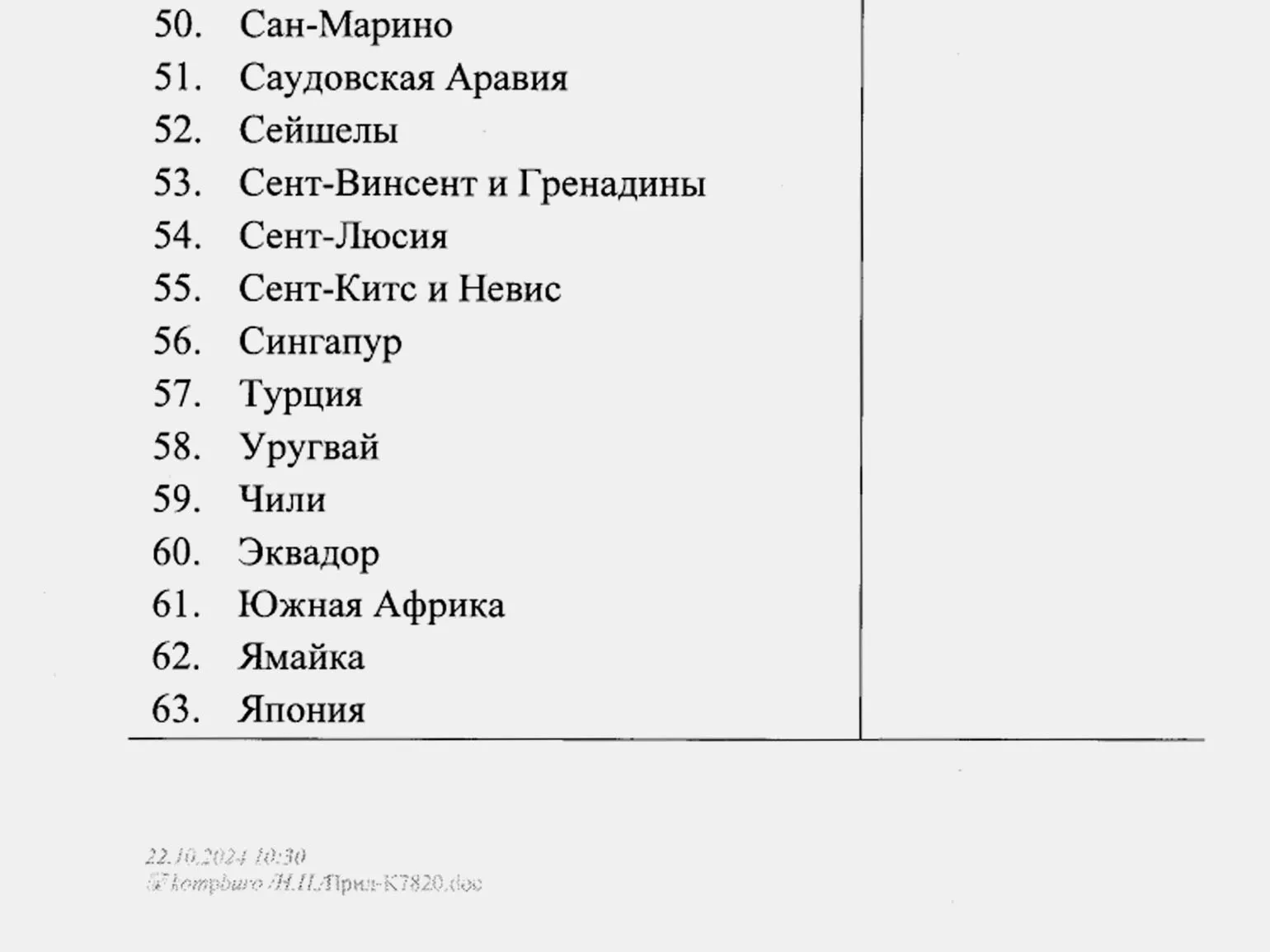

Changes in the FTS white list: key facts for 2025

The new Order of the Federal Tax Service of Russia dated October 30, 2024 No. ED-7-17/916@ comes into force on December 31, 2024. This document updates the whitelist of countries with which the automatic exchange of financial information takes place. The changes to the list are aimed at enhancing the transparency of tax processes and increasing the level of international cooperation in the area of financial control. The updated list of countries will facilitate a more effective exchange of data on the financial assets of individuals and organizations, which, in turn, will help prevent tax violations.

The updated whitelist of partner countries has been reduced. It now includes Armenia, Cameroon, Rwanda, Jamaica, and the territory of Niue. At the same time, 26 countries of the European Union have been excluded from this list. This change may impact international cooperation and trade between these countries and their partners.

To view the full list of countries and territories included in the Federal Tax Service (FTS) whitelist, you can visit the appendix to the order, available on the official online legal information portal.

The automatic exchange of financial information is carried out using special technologies and systems that allow countries to exchange data on taxpayers, financial accounts, and other financial assets. This process involves the use of standardized data formats, such as the Common Reporting Standard (CRS) and FATCA, which ensure compatibility across different jurisdictions.

Automatic data exchange systems operate on the basis of pre-agreed international agreements that establish rules and procedures for processing and transferring information. Participants in the process, including banks and financial institutions, collect the necessary data on their clients and transmit it to the tax authorities of their country. The information is then processed and transferred to other countries, which allows tax authorities to monitor compliance with tax obligations.

This exchange helps increase the transparency of financial transactions and combat tax evasion. The automatic exchange of financial information helps countries identify hidden assets and income, which in turn strengthens tax compliance and promotes fair taxation at the international level.

The automatic exchange of financial account information is carried out in accordance with the Multilateral Competent Authority Agreement (MCAA) and the Single Reporting Standard (CRS), which were developed by the Organisation for Economic Co-operation and Development (OECD). These international standards are aimed at increasing the transparency of financial transactions and combating tax evasion. They ensure the exchange of data between countries to monitor and control the tax liabilities of individuals and legal entities, which contributes to more efficient tax administration and compliance with international tax rules.

Tax authorities of participating countries annually exchange standardized data on taxpayer accounts. The transferred information includes information about the account holder, bank name, account number, balance, as well as interest and other income. This mechanism promotes greater transparency of financial transactions and combats tax evasion.

The automatic exchange of information includes the accounting of accounts of both individuals and legal entities, and also provides data on controlling persons of foreign companies. This process promotes greater transparency of financial transactions and combats tax evasion at the international level.

The Impact of the White List of Countries on the Use of Foreign Bank Accounts for Residents of the Russian Federation

Opening a bank account in a country included in the white list of the Federal Tax Service (FTS) provides residents of the Russian Federation with important advantages. In accordance with current legislation, you can receive funds into such accounts without restrictions. However, if your bank is located in a country not on this list, this may lead to serious legal and financial consequences. Therefore, it is important to carefully select the country in which to open an account to avoid potential risks and problems with regulatory authorities.

According to Article 12 of the Federal Law of December 10, 2003, No. 173-FZ "On Currency Regulation and Currency Control," residents may deposit funds into accounts in foreign banks only in countries included in the white list. This rule is an important aspect for conducting international financial transactions and ensures compliance with currency controls. The white list of countries identifies reliable jurisdictions, allowing residents to minimize risks and comply with legal requirements when conducting transactions abroad.

If a Russian resident has a bank account in a country that is not on the white list, they may face restrictions on receiving funds from non-residents. Certain types of receipts are prohibited, including transfers from foreign legal entities and individuals, as well as payments for goods and services. This creates significant difficulties for conducting international financial transactions and requires a careful approach to choosing a bank and country in which to open an account. Residents need to stay informed about current rules and regulations to avoid transfer issues and ensure the security of their financial transactions.

- Income from the sale of property;

- Payment for work performed or services rendered;

- Dividends, coupons, and income from securities transactions;

- Loans and other income prohibited by currency legislation.

When receiving funds to an account in a foreign bank, it is important to consider ways to minimize risks. If the funds came from a country not on the white list, you can transfer these funds to an account in a Russian bank within 45 days of receipt. This will help avoid potential liability for violating currency legislation and protect your financial interests. Consulting with financial consulting professionals can help ensure the transfer process is properly organized and all necessary requirements are met. In today's environment, when many banks are imposing restrictions on transactions with Russia or requiring additional verification, this method of transferring funds may prove ineffective. There is a risk of funds being delayed at the foreign bank, which could result in them not arriving in Russia on time. This can complicate financial transactions and cause additional inconvenience for clients.

Violating currency regulations has serious consequences, including significant financial fines that can reach 40% of the amount of the illegal transaction. Using bank accounts in countries not on the white list is associated with high risks. Therefore, it is important to carefully monitor such transactions and comply with legal regulations. Ignoring currency regulation rules can lead not only to fines but also to criminal liability. Therefore, it is recommended to seek advice from specialists in financial law and currency regulation to avoid negative consequences.

The Impact of Changes in the Federal Tax Service Lists on Controlled Foreign Companies (CFCs): Real-World Experience

Changes in the black and white lists of the Federal Tax Service (FTS) can have a significant impact on the activities of controlled foreign companies (CFCs). In this review, we will analyze several practical examples illustrating how critical the relevance of information is for successful business. Current information about a company's blacklisting and whitelisting can impact its tax liabilities and reputation, making monitoring these lists an important part of strategic management for all CFCs.

A Russian businessman owns a controlled foreign company (CFC) registered in Austria. Recent changes in tax legislation, including the blacklisting of Austria by the Russian Federal Tax Service (FTS), deprive him of the opportunity to take advantage of the CFC's profit tax exemption based on the effective tax rate. This could lead to significant financial losses for the business, as tax liabilities increase and the attractiveness of foreign investment decreases. It is important to consider these risks when planning a tax strategy and managing international assets.

An individual who is a tax resident of Russia controls a company in Germany, which conducts business in Russia. In this case, when dividends are paid along the chain "Russian company → German company → individual in Russia," this individual faces the problem of double taxation. This occurs because it cannot account for taxes paid in Russia, which complicates financial calculations and reduces investment returns.

A resident of the Russian Federation has an account in a Swiss bank. The removal of Switzerland from the Federal Tax Service's whitelist increases the risks for account holders. Transfers to this account from non-residents that do not meet Russia's currency requirements may result in fines and other sanctions. This circumstance requires a careful approach to financial transactions and compliance with the law to avoid negative consequences.

A Russian resident who owns a company registered in the United States will face new requirements starting in 2025. Since the United States is on the Federal Tax Service's (FTS) blacklist, the notification of controlled foreign companies (CFC) will require not only financial statements but also an auditor's report. This will significantly complicate the tax compliance process and may entail additional costs for company owners. It is important to prepare for these changes in advance to avoid problems with tax authorities.

These examples clearly demonstrate the importance of monitoring changes in the Federal Tax Service (FTS) lists and the need to adapt business processes to new requirements. Regular consultations with tax specialists and the use of up-to-date information sources will help avoid mistakes and ensure compliance with current legislation. This will not only minimize risks but also optimize business processes, which will ultimately have a positive impact on the company's financial performance.

Recommendations for Minimizing Risks and Penalties When Managing Offshore Accounts and CFCs in 2025

To minimize risks and avoid financial sanctions when using offshore accounts and controlled foreign companies (CFCs), it is important to adhere to a number of recommendations. First of all, carefully check the legal cleanliness and reputation of the offshore jurisdictions with which you plan to work. Ensure full compliance with the laws of both your home country and the country where your company is registered. Maintain transparent records of all financial transactions and documents related to offshore accounts. Regularly update information on tax requirements and legislative changes to avoid unforeseen consequences. Consider consulting with professional lawyers and tax advisors to stay informed of current risks and obligations. Timely compliance with all regulatory requirements will help protect your interests and reduce the likelihood of financial sanctions. Check current Federal Tax Service lists. Before opening a new account or registering a CFC, make sure the chosen jurisdiction is not on the Federal Tax Service's blacklist. Having a bank account in a whitelisted country will allow you to legally receive funds from non-residents of the Russian Federation. Comply with currency laws. It is important to monitor permitted transactions and avoid illegal transfers to foreign accounts. Transfer funds to the Russian Federation in a timely manner. If your account is opened in a country on the Federal Tax Service's blacklist, transfer incoming funds to a Russian account within 45 days to avoid fines for illegal currency transactions.

By following the recommendations provided, you can successfully manage your international business while complying with Russian legislation. This will help avoid unexpected fines and ensure the legality of your financial transactions, which in turn will increase the trust of partners and clients. Proper compliance with rules and regulations will allow you to minimize risks and create a sustainable foundation for the further growth and development of your business in the international arena.

Starting a Business in 2024: 5 Steps to Success

Want to start a business in 2024? Learn 5 key steps for a successful start!

Learn more