Contents:

Life can be made better! Master an in-demand profession, earn more, and enjoy your work.

Find out more

Marat Enanov, Financial Director of the Orange loyalty service, shared recommendations for proper personal budget planning. Effective financial management requires a thorough approach and awareness. It is important to start by analyzing current income and expenses to understand where the funds are going. Then you should set financial goals, such as saving for large purchases or creating an emergency fund. It's recommended to divide your budget into fixed and variable expenses, which will allow for more precise spending control. It's also worth factoring in unexpected expenses by building a reserve into your budget. Regularly reviewing your financial plan will help you adapt to changes in income and expenses, making personal finance management more effective. Running a business without clear plans, calculations, and strategy is like managing a personal budget without taking financial realities into account. This approach can lead to significant losses and even bankruptcy. However, if you apply business tools to your everyday life, you'll notice that PnL reports (profit and loss statements) can be effectively used to manage personal finances. Furthermore, even simple activities like going out for a coffee have their own unit economics, which allows you to analyze expenses and income. Using these tools in your daily life will help you optimize your financial flows and make more informed decisions, which in turn will lead to improved financial health in both business and personal life.

In this article for the Skillbox Media "Money" editorial team, I will share information on key aspects of financial management. We will examine important strategies that will help you optimize your budget, improve your financial literacy, and learn how to manage your funds effectively. We will also discuss the main mistakes people often make when planning their finances and offer practical recommendations for avoiding them. It is important to understand that proper financial planning not only improves your current financial situation, but also creates a reliable base for future investments and savings.

- What is PnL and how to use it for budgeting;

- How cash flow can help you stop borrowing until payday;

- How to find out the payback period of a coffee machine;

- How to correctly calculate expenses.

What is PnL and how to use it for budgeting

Every entrepreneur strives to optimize their expenses and increase income. Successful implementation of these goals contributes to business growth, opens up new opportunities and allows the owner to put funds aside for other projects or create a reserve fund. In order to control financial flows and determine the most profitable areas, businessmen use the analysis of the PnL (Profit and Loss) indicator. This tool helps identify where funds are going and which aspects of the business are generating the most profit, which in turn facilitates more effective management and planning.

PnL (profit and loss, pronounced "pee-neel") is a key financial metric that reflects the difference between all income and expenses for a given period. This information is the basis of the PnL (profit and loss) report. The main purpose of this report is to determine whether a business was profitable or unprofitable, as well as to analyze the factors that influenced financial results. Proper understanding and interpretation of PnL helps businesses make informed decisions, plan for the future, and optimize costs.

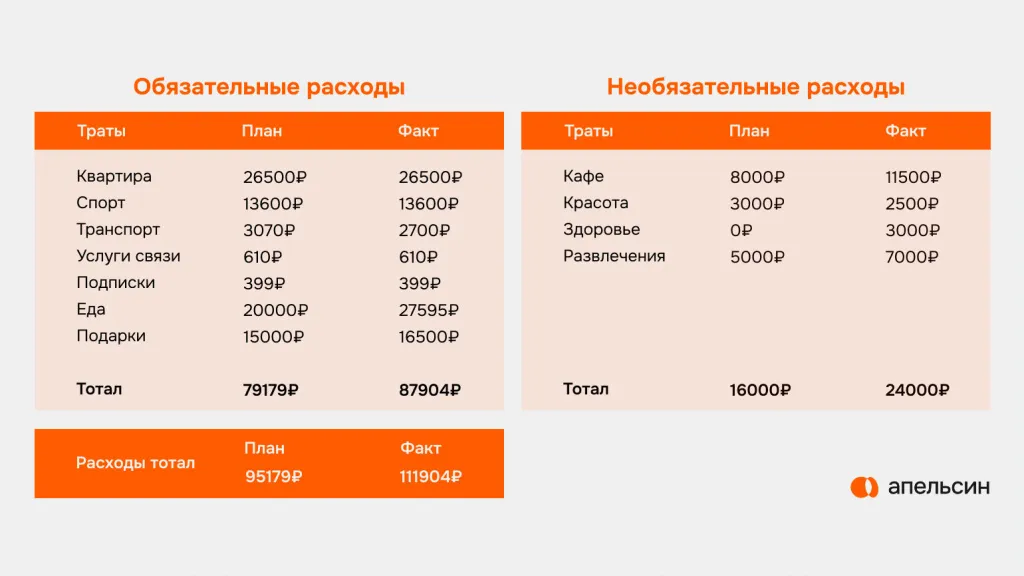

Using PnL (profit and loss) in personal budgeting can significantly improve financial literacy. Start by recording all income and expenses daily, which will help you get a complete picture of your finances. For easier analysis, it is recommended to divide income and expenses into categories, such as housing, food, transportation, and entertainment. This will allow you to identify the main expense items and optimize your budget. Regular data analysis will help you make more informed financial decisions and achieve your goals.

- Income. Here, you need to account for all sources of income: salary, part-time work, selling old items, debt repayment, cashback, and others.

- Expenses. This section should include both mandatory and unexpected expenses—for example, mortgage and utility payments, food purchases, transportation costs, subscriptions, medical services, or repairs to broken equipment. It's easiest to track this in a banking app, where expenses are already categorized.

You can track your finances in a way that's convenient for you. For example, you can record your expenses and income in a diary or use Excel spreadsheets for a more structured approach. There are also specialized smartphone apps, such as Money Flow and CoinKeeper, that help you effectively manage your budget and track your cash flow. The choice of accounting method depends on your preferences and goals, but it is important to update data regularly to achieve the best results in financial management.

At the end of the month, it's important to analyze each category to summarize. You need to determine your total income and expenses. To do this, subtract your total expenses from your total income for the month. This approach will help you better understand your financial situation and identify areas for improvement in the future.

Profit is an amount that you can use as you see fit. You can decide to put it aside for savings or spend it on something that brings you pleasure.

If you're facing negative financial indicators, it's time to activate your "entrepreneurial vision." Analyze your expenses and identify items that can be reduced or eliminated altogether. Consider opening new sources of income that will help improve your financial situation. Don't forget to regularly review your strategy, repeating this process every other month to evaluate the effectiveness of the measures taken.

PnL can greatly assist in analyzing business cash flows. First of all, it provides a clear picture of the expense structure. For example, you might discover that your monthly expenses on prepared meals amount to 12,000 rubles, while 8,000 rubles are spent on subscriptions and courses, many of which remain unused. This understanding will allow you to optimize your budget, cut unnecessary expenses, and redirect funds to more effective tools or services, which will ultimately improve your business's financial health. By reducing your monthly expenses by 14,000 rubles, you can free up funds for other purchases. Over the course of a year, this will allow you to save 168,000 rubles, which is enough to organize a vacation. Optimizing your budget will not only improve your financial situation but also create opportunities for new experiences and relaxation.

How Cash Flow Can Help You Stop Borrowing Until Payday

Some people have a high income but don't control their spending, which leads to a shortage of money by the end of the month. Despite a conscious attitude towards finances and avoiding impulse purchases, they are forced to resort to temporary financial solutions, such as borrowing from friends or using credit cards. This emphasizes the importance of not only income generation but also proper personal finance management to achieve financial stability.

In business, there is a concept of a "cash gap," which refers to a situation when financial obligations need to be met, but there is not enough cash. This problem often occurs due to insufficient financial planning and improper accounting of income and expenses. Proper cash flow management and forecasting financial needs will help avoid a cash gap and ensure stability in the business.

To reduce or completely eliminate cash flow gaps, it is important to closely monitor financial flows. The key solution is to track your cash receipts and expenses. This requires not only recording the expected amounts of income and expenses but also specifying the dates of expected receipts and expenses. This approach will help you plan your budget more accurately and avoid financial difficulties. Keeping detailed records will allow you to anticipate potential gaps and take steps to address them in advance. Using this approach, you can plan your financial obligations in advance. For example, you might need to pay your rent or mortgage on the 10th. This will allow you to set aside the necessary amount in advance or limit your spending until that date, ensuring you have the necessary funds in your account to cover the payment. This method of financial management will help to avoid delays and financial difficulties.

Accounting Cash flow, along with the profit and loss statement (PnL), is an important tool for analyzing the financial health of a business. It allows you to determine whether there are sufficient funds to cover current expenses. To do this, subtract the total amount of expenses from the amount of income. If the result is positive, this indicates the availability of available funds that can be used for savings or reinvestment in the business. Proper accounting of cash flow helps avoid financial difficulties and contributes to the sustainable development of the company.

How to Find the Payback Period of a Coffee Machine

Let's say you buy a cup of coffee for 300 rubles every day on the way to work. This small expense may not seem significant compared to buying a coffee machine, which costs several tens of thousands of rubles. However, if you calculate the payback period (PP), you can understand that a large investment in a coffee machine can quickly pay off. Effectively analyzing these costs will help you make more informed choices between everyday purchases and long-term investments.

How to calculate the payback period? Let's look at a specific example. The price of one cup of coffee is 300 rubles. Let's assume that you buy coffee every workday. If there are 22 workdays in a month, then your monthly coffee expenses will be 6,600 rubles, which is calculated using the formula: 300 rubles × 22 days = 6,600 rubles. Calculating the payback period will help you understand how long it will take to recoup your investment in coffee, which is useful for budgeting.

By purchasing a coffee machine and making coffee yourself, you can significantly reduce the cost of one cup of the drink. Below are approximate prices for making coffee at home.

The amount of coffee and milk used for preparation will allow you to make about 120 cups of coffee. As a result, the cost of one cup of homemade coffee will be 35 rubles, which is calculated using the formula: (2400 + 1800) / 120 = 35. The savings on each cup reach 265 rubles, since the price of purchasing one cup of coffee in a cafe is 300 rubles, and the homemade version costs only 35 rubles.

Now you can calculate how quickly a coffee machine will pay for itself. Let's say you're planning to purchase a model priced at 33,000 rubles. To calculate the payback period, we use the formula: divide the cost of the coffee machine by the savings per cup of coffee. In this case, considering an inexpensive coffee machine and consumables, the calculation would be: 33,000 rubles divided by 265 rubles, which equals 125 cups of coffee. If you drink a cappuccino every workday, your investment in a coffee machine will pay for itself in approximately five months. Therefore, purchasing a coffee machine will not only improve the quality of your coffee but also allow you to save significantly on daily expenses.

These are approximate calculations. You can choose a more expensive coffee machine model, use different types of milk, beans, or filtered water. These factors will affect the payback period of the coffee machine.

How to calculate expenses correctly

Determining the cost of lunch, a trip to the country, or a fitness class may seem simple. However, for an accurate estimate, you need to delve into the details. This is where unit economics comes to the rescue. This tool is useful not only for entrepreneurs, but also for analyzing a personal budget. Unit economics allows you to understand how much your habits and lifestyle really cost. Understanding these costs will help you optimize spending and make more informed financial decisions.

Lunch at a cafe for one person costs 1,200 rubles. Thus, for a family of four, the total expenses will be 4,800 rubles.

Home-cooked meals are, on average, 2.2 times more cost-effective. Cooking at home not only saves money, but also allows you to control the quality of ingredients and monitor the nutritional value of your diet. Choosing home-cooked meals promotes healthier eating and reduces spending on eating out.

It's important to focus on the unit cost rather than the total cost. This helps avoid the illusion of savings. For example, you might spend 5,000 rubles on a monthly gym membership, but if you skip half your workouts and only go four times, the real value of your investment is significantly reduced. This approach allows you to better understand the return on investment and increase motivation for regular exercise. By analyzing unit costs, you can make more informed decisions and achieve your desired results.

The cost of one session is 1,250 rubles if you divide the total cost of 5,000 rubles by four sessions. However, purchasing individual sessions at 800 rubles is a more economical option. This allows you to save money and make classes more accessible.

The Key to Personal Finance Planning in 4 Points

- To better manage your money, you need to understand how much you earn and how much you spend. The PnL ratio, which reflects the difference between income and expenses, helps with this. If you spend more than you earn, it’s worth reviewing your expenses or thinking about additional income.

- Even with a high income, you can encounter what is called a cash gap in business - a situation when you need to pay now, but the money will come later. To avoid this, it is important not only to calculate income and expenses, but also to track exactly when money comes in and goes out. Such accounting helps you see in advance what you may not have enough funds for and adjust your plans in time.

- Sometimes large purchases seem unprofitable compared to regular small expenses. But if you calculate the payback period, you can understand how long it will take for such investments to pay for themselves. This approach helps you make smarter decisions and save significantly.

- Unit economics helps you understand how much a particular habit or part of your lifestyle really costs. It allows you to, instead of looking only at the total amount, estimate the cost of one unit - for example, one gym session or one taxi ride.

We present to you additional materials from Skillbox Media that you may find useful.

- Cryptocurrency investments: what you need to know and how to start without losing money

- How to understand that you are being called by scammers, and how to protect yourself from phone scams

- Rare Russian coins that you may have in your piggy bank

- 7 ways to earn passive income with almost no risk

- Understanding economics is important. We'll help you understand how everything works