Contents:

Practical course: "Personal finance: investments and trading"

Learn more

Anna Dengina, author of financial development programs and head of the Financial Health service of the National Center for Financial Literacy, participated in writing this article. Anna is also a speaker of the Skillbox course "Finliteracy: learning to manage a budget, save and invest", where she shares her knowledge about proper financial management, savings and investments. Her experience and expertise in financial education make the article more valuable and informative.

A financial plan can be created not only for business but also for personal needs. If you have goals, such as purchasing real estate or accumulating personal wealth, it is important to develop a plan to achieve them. Such a plan will serve as a roadmap that will help you move from your current financial situation to your desired outcome. Creating a proper financial plan includes analyzing your income and expenses, setting priorities, and setting a timeline for achieving your goals. This will allow you to more effectively manage your finances and achieve your goals.

In this article from the Skillbox Media "Money" editorial team, you will find information on the key aspects of financial literacy. We will discuss how to properly manage personal finances, plan a budget, and invest funds to achieve financial independence. You will also learn about modern tools and resources that will help you effectively manage your finances, as well as common mistakes to avoid. This material will be useful for anyone who wants to improve their financial situation and learn to make informed financial decisions.

- What is a personal financial plan;

- How to create one;

- What tools are useful for maintaining a plan;

- What mistakes are made when creating one.

What is a personal financial plan and why do you need one?

A personal financial plan is a key tool for achieving your financial goals. This document contains a strategy that helps you structure your finances and identify specific steps to achieve your goals. As part of a financial plan, it is necessary to clearly define not only your goals, but also the consistent actions that will help you achieve these goals. Creating a personal financial plan is available to everyone, regardless of income level, which makes it an important tool for managing personal finances and improving financial well-being.

According to research, having a financial plan significantly improves financial literacy and overall well-being. People who set long-term financial goals are more likely to purchase life insurance, save significantly, and generally have a higher income relative to their expenses. Creating a financial plan promotes more conscious financial management and helps you achieve your goals. Having a financial plan significantly simplifies personal finance management. Such a plan facilitates more effective budgeting, helps you prioritize spending and savings, and allows you to better assess financial risks. Systematic planning allows you to control your financial goals, whether it's buying real estate, education, or building an emergency fund. Furthermore, a financial plan serves as a basis for making informed decisions, which ultimately leads to greater financial stability and confidence in the future. It's important to closely track your income and expenses. You need to clearly understand how much money is coming into your account each month, as well as what these funds are spent on and in what amounts. This will help you better manage your budget and make informed financial decisions. A systematic analysis of your financial flows will allow you to identify unnecessary expenses and optimize spending, which in turn will improve your financial situation. Saving is an important step in building financial stability. This may include creating a safety net, saving for major purchases, or building retirement savings. Regular saving helps protect against unexpected expenses and allows you to achieve your planned financial goals. Creating strategies for saving, such as automatic transfers to a savings account, can significantly simplify the process and make it more efficient. Investing is a key tool for creating passive income and increasing personal capital. The right investments can form the basis for future major purchases, such as a home or children's education. By investing, you not only protect your savings from inflation but also give them the opportunity to grow. This allows you to ensure financial stability and achieve your long-term goals. Risk protection is an important part of a financial strategy. One way to minimize risk is to take out insurance, which will provide financial protection in the event of unforeseen circumstances. You should also consider setting up reserve accounts to set aside funds to cover emergency expenses. These measures will help ensure your financial security and prepare you for potential difficulties.

Debt management is an important aspect of financial planning. To effectively manage loans and personal debt, it is necessary to develop a convenient and favorable payment schedule. This approach will allow you to repay debts on time, avoiding penalties and deterioration of your credit history. Proper allocation of financial resources and control over payment terms will help maintain financial stability and improve overall well-being.

Planning timeframes vary from short-term, covering a few months, to long-term, which can be 10 years or more. The right approach to planning allows you to effectively manage resources and achieve your goals within the specified time frame.

How to Create a Personal Financial Plan

Creating a personal financial plan requires a number of steps, from understanding its importance to choosing the right financial instruments. In this article, we'll take a detailed look at each step of the process of creating an effective financial plan.

Defining life goals is a key step in planning your financial future. Before setting financial goals, you need to clearly understand what you want to achieve within a year, five, or ten years, as well as the lifestyle you want to lead. This understanding will help you formulate specific financial objectives that will help you achieve your long-term goals and achieve your desired standard of living.

Many people dream of starting a family and living in a spacious apartment or country house. Important aspects for them include owning a car and the ability to provide their children with a quality education in a good school and participating in sports clubs. For others, career development and the opportunity to open or expand their own business become a priority. All of these desires directly influence the formation of financial goals and the strategy for achieving them. Proper financial planning and management will help you realize your dreams and ensure a stable future.

Formulating financial goals is an important step towards financial independence. A financial goal is a specific and measurable result that can be achieved with money. Examples of such goals include buying an apartment, a car, or renovating a home. Clearly defined financial goals help create a clear action plan and simplify the process of managing your personal budget.

Goals are classified according to the time frame for their achievement. There are short-term, medium-term, and long-term goals. Short-term goals are usually achieved within a few days or weeks; they allow you to quickly see results and maintain motivation. Medium-term goals require several months to implement and help in planning larger tasks. Long-term goals can take years and often serve as the basis for a strategy for achieving success. Correct goal setting by time frame helps optimize efforts and effectively manage time.

- short-term - up to one year;

- medium-term - 3-5 years;

- long-term - five years or more.

In financial planning, it is important to set several goals and effectively allocate funds between them. For example, the goal "save for a vacation abroad" is considered short-term, while "build retirement savings" is a long-term goal. Proper resource allocation will help achieve both goals, ensuring financial stability and the ability to enjoy life now and in the future.

The SMART methodology is an effective tool widely used in business planning. It suggests that goals should be specific, measurable, achievable, relevant, and time-bound. Using this methodology allows you to clearly define areas of activity and evaluate progress towards achieving these objectives. The main advantage of SMART is that it helps focus on tangible results and minimize the risks associated with uncertainty. Thus, using the SMART method contributes to more effective project management and increases their success.

Simply writing down "I want to buy an apartment" in a notebook is not enough. It is important to carefully calculate the property value taking into account inflation, determine the planned purchase timeframe, and assess the availability of your own funds. It is also necessary to analyze whether a mortgage will be required and take into account all financial aspects. In the next section, we will look at these issues in more detail.

Content readability and quality play an important role in SEO. Optimizing your text helps improve its visibility in search engines and attract more visitors to your website. To achieve this, you need to consider relevant keywords and use them organically throughout the text. It's also important to create unique and informative content that addresses user needs and solves their problems. Regularly updating information and adding new materials helps keep your website relevant. Don't forget about the importance of internal and external link building, which also impacts SEO rankings.

Read also:

Learning about SMART goals is essential, as successful goal setting is difficult without it. The SMART methodology helps formulate goals so that they are specific, measurable, achievable, relevant, and time-bound. Using this system not only clearly defines the direction of work but also improves the efficiency of task completion. It's important to understand how to formulate SMART goals correctly so that they contribute to the desired results and provide clarity at every stage of the project. Without this structure, the task-setting process can be ineffective and confusing.

To achieve a financial goal, it's important to calculate the required savings. At this stage, you should determine how much money you need to set aside regularly to achieve your plan within the established deadline. For example, if your goal is to purchase a car worth 2 million rubles in five years, you will need to save at least 33,333 rubles monthly. It is recommended to increase this amount based on inflation and possible unexpected expenses to ensure successful achievement of your goal.

The first step is to evaluate whether it is possible to save the required amount from your own funds or whether a loan is worth considering. For example, when planning a real estate purchase, it is important to keep in mind that saving slowly may not keep up with market price increases. In such situations, a mortgage loan may be a more practical solution than long-term savings. This will allow you to purchase the property faster and avoid possible financial losses due to increased value.

To effectively manage your finances, you need to carefully analyze all current income and expenses. Income should include salary, earnings from part-time jobs, and passive income, such as rental income or interest on bank deposits. Expenses cover all types of expenses, including housing and utility bills, as well as impulse purchases, vacations, and entertainment. Understanding your full financial picture will help you optimize your budget and improve your financial situation. If your current income doesn't allow you to cover all your expenses and save for your financial goals, it's important to start by optimizing your budget. Reducing unnecessary expenses and increasing your income will be key steps toward financial stability. Consider finding a job with a higher salary, which can significantly improve your financial situation. It's also worth considering creating passive income streams, such as real estate investments or financial assets, which will allow you to earn additional funds without constant effort. These measures will help you not only cope with current financial difficulties but also ensure savings for future goals.

Reworked text:

Also study:

Passive income is the ability to earn money without constant active participation. There are many ways to generate passive income that can help you financially stabilize and provide additional cash flow. Let's look at seven effective methods for creating passive income.

The first method is investing in stocks and bonds. Purchasing securities allows you to receive dividends and interest without the need to manage assets on a daily basis. Choosing stable companies with a good reputation can provide a reliable income.

The second method is real estate. Investing in rental properties provides the opportunity to receive regular rental payments. Choosing the right location and type of property can significantly increase profitability.

The third method is creating online courses. If you have expertise in a specific field, you can develop a course and sell it on learning platforms. This will create a stable income from sales as long as your course remains relevant.

The fourth method is writing books or e-publishings. Copyrights for your works can generate royalties long after they are published. Choosing popular topics and properly promoting your work will help increase sales.

The fifth method is creating a blog or YouTube channel. Earning money from advertising, affiliate programs, and sponsorship contracts can become a stable source of income. The main thing is to attract an audience and regularly update the content.

The sixth method is investing in crowdfunding platforms. You can invest money in various projects that promise a return with interest. This requires careful analysis, but can bring in a good income.

The seventh method is creating passive income through automated business models. For example, online stores with dropshipping or selling digital products require minimal involvement after setup.

Each of these methods can be an effective source of passive income. It is important to choose one that aligns with your interests and financial goals. Passive income requires initial effort, but over time it can provide you with financial freedom and stability.

Budget analysis is an important step in managing your personal finances. Whether to record every little detail, such as coffee or subway fare, depends on individual preference. Some people prefer to track every penny to get a comprehensive overview of their spending, while others prefer to summarize their expenses. The choice of accounting method depends on each person's goals and habits. It's important to remember that systematic budget analysis allows for better financial control and cost optimization.

To thoroughly analyze your budget, it's enough to review your expenses and income for 2-3 months. However, to get a complete picture and track seasonal changes in spending, it's recommended to analyze data for the year. This will help you identify that expenses may increase in the summer due to vacations and preparing children for school, and in December due to buying New Year's gifts for family and friends. This approach to managing cash flows helps you better plan your budget and avoid unexpected expenses.

Checking your risk tolerance is a key aspect of financial planning. When setting goals, it's important to consider potential force majeure events, such as job loss or health problems. It's important to assess whether you can maintain a comfortable standard of living in the event of a temporary loss of income or unexpected large expenses. It's also important to analyze how long your savings will last in such circumstances. This approach will help you manage your finances more effectively and minimize the negative consequences in difficult situations.

The optimal solution is to create a financial safety net capable of covering essential expenses for 3-6 months. It's also important to take out life and property insurance for yourself and your loved ones to provide additional protection in unexpected situations. This will help reduce financial risks and increase stability during difficult times.

If you don't have emergency savings, building one should be your top financial goal. Start by building an emergency fund that covers at least three months of your living expenses. Once you reach this goal, you can move on to the next steps of managing your finances.

Budgeting and optimizing are key aspects of financial well-being. Regularly saving for predetermined goals contributes to financial stability. Effective budget management and wise income allocation will help you in this process. There are many approaches to budgeting, and there are no strict rules. One common method is the 50/30/20 rule, which suggests distributing your income as follows: 50% for necessary expenses, 30% for personal desires, and 20% for savings and debt repayment. This method not only allows you to control your expenses but also provides a financial safety net, which is especially important in an unstable economy.

- 50% of income - for essential expenses, such as housing, food, and utilities.

- 30% - for entertainment and hobbies.

- 20% - for savings and investments.

You can use different proportions or distribute the budget across more categories, depending on your individual needs and goals.

At this stage, it is important to analyze your behavior and actively work to improve it in order to follow the intended financial plan. This can be difficult, especially if you previously did not have the habit of controlling your spending or you have difficulty giving up impulsive purchases. Understanding your financial habits and adjusting them will help you achieve your goals.

Compare your lifestyle with the goals set in the financial plan and adjust your financial habits based on this. For example, if you only have 10,000 rubles per month left for investments and need more to reach your goal, review your expenses and cut unnecessary spending. Also consider ways to increase your income to achieve your desired financial results. Investing is an important tool for protecting your funds from inflation and generating passive income. The simplest options are bank deposits and savings accounts. These instruments allow you to preserve capital and earn fixed interest. More complex investment instruments, such as federal loan bonds (OFZ) and stocks, can offer higher returns but require more analysis and market understanding. Investing not only helps protect your money but also grow it, which is an important step toward financial independence. Optimizing taxes and taking deductions, such as for education and medical services, are important steps to improving financial efficiency. The funds saved can be used for investments to grow your capital, or set aside for achieving specific goals. Considering all available tax deductions will not only help reduce your tax burden but also ensure financial stability in the future.

Review your plan regularly. Every 3-6 months, it is important to evaluate your progress and make any necessary adjustments to your strategy. This is especially important if your income increases or your goals change. This approach allows you to stay on track and adapt to new conditions.

What services can I use to maintain a personal financial plan?

There is no universal tool for creating a financial plan, as everyone approaches this process individually. There are many different methods and tools that can be used to effectively manage personal finances. These can be spreadsheets, specialized applications, or even simple notebooks. The main thing is to choose the method that best suits your needs and lifestyle. The right tool will help you track your income and expenses, plan a budget, and achieve your financial goals.

A financial tracking app like Monefy or CoinKeeper allows you to effectively track your expenses and income. These tools are ideal for the second stage of creating a financial plan. Users can quickly record all purchases, categorize them, and get visual information about their finances. The ease of use and functionality of such apps help you better control your budget and achieve your financial goals.

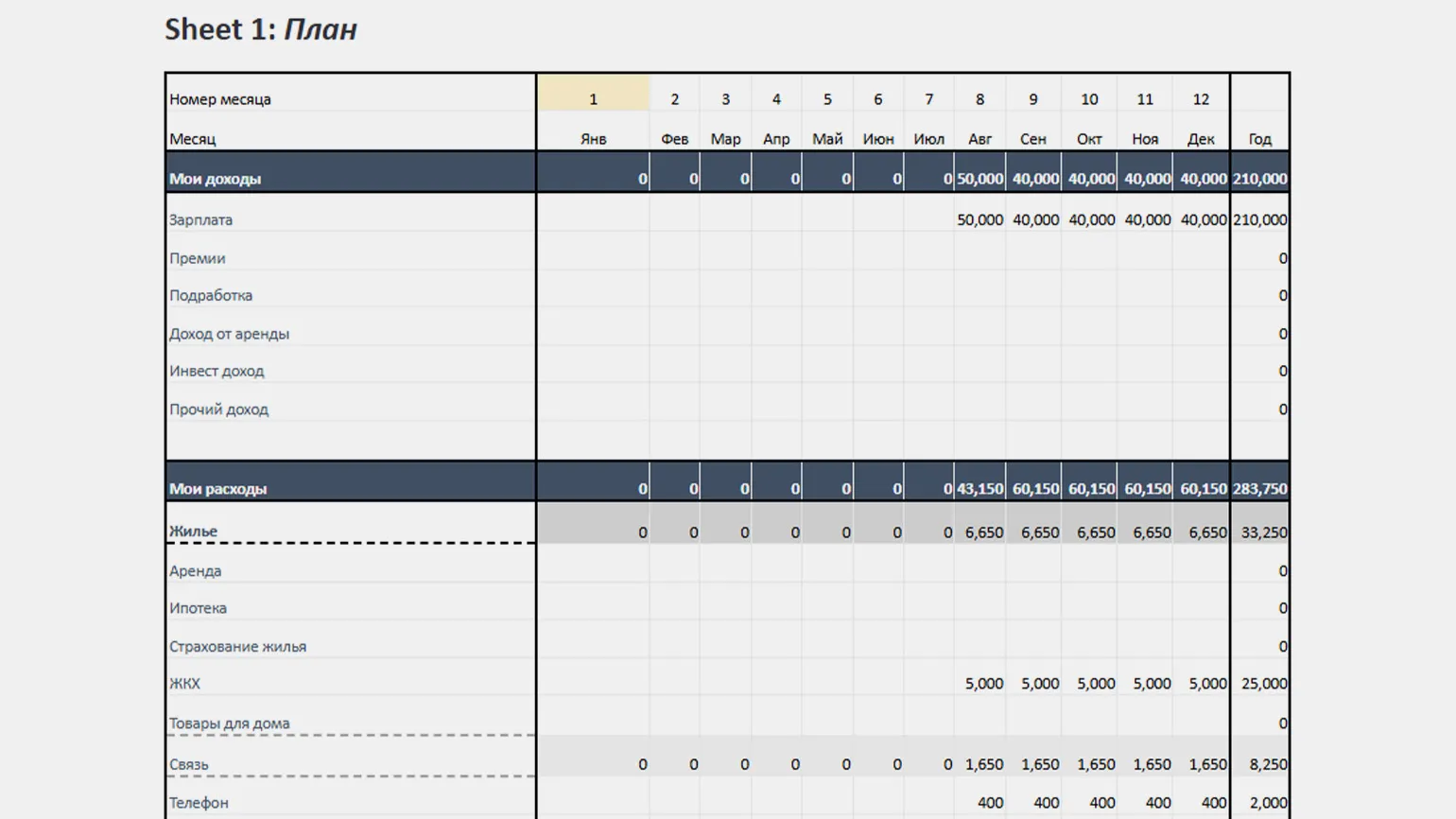

Excel spreadsheets are an indispensable tool for financial management, especially after you've defined your budget and set financial goals. With their help, you can create a custom spreadsheet and set up formulas for automatic calculations, which significantly simplifies the process of tracking your expenses and income throughout the month. This will allow you to control how much money remains until you reach your goals. Using Excel for financial planning helps you manage your budget more effectively and achieve your desired results.

This resource offers a spreadsheet template for effective budget control. Download it to simplify financial planning and expense tracking. This tool will help you organize your finances and achieve your financial goals.

Read also:

Excel is a powerful spreadsheet program developed by Microsoft. It is widely used for data analysis, bookkeeping, graphing, and information visualization. Excel provides users with tools for organizing and manipulating data, making it indispensable in business, scientific research, and everyday life.

Working in Excel begins with creating a new table, where you can enter data into cells arranged in rows and columns. The program supports a variety of data formats, including text, numbers, and dates. Excel offers a variety of functions that allow you to perform mathematical calculations, statistical analysis, and financial calculations. Among the most popular functions are SUM for summing values, AVERAGE for calculating the average, and VLOOKUP and HLOOKUP for searching data in tables.

In addition, Excel offers the ability to create charts and graphs, which helps visualize data and make it more understandable. Users can apply conditional formatting to highlight specific values, as well as use filters and pivot tables to simplify the analysis of large amounts of information.

Using macros and VBA (Visual Basic for Applications), you can automate routine tasks and extend Excel's functionality, making your work with the program even more efficient. Excel also supports collaboration, allowing multiple users to edit a single spreadsheet simultaneously.

In conclusion, Excel is a versatile tool suitable for a wide range of data-related tasks. Understanding the program's key features and capabilities will significantly improve your productivity and data management.

Mistakes People Make When Creating a Financial Plan and How to Avoid Them

Mistakes in financial planning can occur at any stage of the process. It is important to understand which of the most common ones to avoid unpleasant consequences. In this article, we will consider the key mistakes that can negatively impact your financial goals.

The lack of a systematic approach to financial planning leads to inefficiency and uncertainty. A financial plan should not just be a wish list, but a detailed, step-by-step strategy. Without clear stages, deadlines, and specific tools, achieving goals remains just dreams. The correct approach to financial planning includes a clear understanding of your goals and a realistic determination of the resources needed to achieve them. This will allow you not only to effectively manage your finances but also minimize the risks associated with their implementation.

Rigid goals without flexibility can negatively impact the success of a project. Every plan is subject to risk, and unforeseen circumstances can derail it. Therefore, it's important to regularly review your budget and timeline to adapt to changes in income or market conditions. Flexibility in project management allows you to respond promptly to challenges and maintain control over processes, which contributes to more effective achievement of your goals.

When choosing financial products, it's important to consider your goals and risk level. Investing in stocks is not advisable if you plan to use the money within a year, as their value can fluctuate significantly, leading to losses when selling. Furthermore, relying solely on bank deposits to save for retirement is also unprofitable, as inflation can significantly reduce the real value of your savings. The right approach to financial investments involves balancing risk and return, as well as carefully planning your timeframe and goals.

An excessively large safety net can be ineffective. It is recommended to have savings sufficient to cover expenses for 3-6 months. Keeping all savings in cash or bank deposits leads to a loss of return due to inflation. The optimal strategy is to diversify assets to preserve and grow capital, rather than simply hoard it in inefficient forms.

The lack of a financial cushion becomes a serious problem. Without sufficient reserves, even small expenses, such as dental work or car repairs, can lead to the need to take out loans. This leads to a loss of savings and financial instability. Creating a financial cushion helps avoid debt and provides confidence in the future.

A short planning horizon, focused only on the next year or two, does not allow for important long-term goals, such as children's education or saving for retirement. Ignoring these aspects can lead to financial difficulties in the future. Therefore, it is important to consider your financial strategies taking into account not only current needs but also future obligations and goals. Long-term planning allows you to manage your resources more effectively and achieve sustainable financial well-being. Ignoring tax breaks and deductions can lead to significant financial losses. Tax deductions, subsidies, and specialized banking programs can significantly reduce your financial burden and protect you from future overpayments. Using these tools allows you to optimize your expenses and improve your financial situation. Don't miss out on the opportunity to take advantage of available benefits, as they can play a key role in your budget. A careless approach to loans can lead to serious financial consequences. Using credit for fun or ignoring overpayments creates the risk of falling into debt. However, it's important to remember that fearing a mortgage with a 5% interest rate when inflation is 7% is also a mistake. It's important to analyze financial risks and make informed decisions to avoid unpleasant consequences and ensure financial stability.

The Key to a Personal Financial Plan in 3 Points

- A personal financial plan is a document that describes financial goals and how to achieve them. A plan makes it easier to control your budget and save money for different purposes.

- Building a personal financial plan is a whole system where consistency is key. First, you need to set measurable goals and calculate how much time and money you need to achieve them. Then, create a foundation for financial stability—a safety net—and learn to manage your income and expenses. To implement a financial plan, you need financial products: loans, deposits, and investment instruments. The plan should be reviewed every few months to make adjustments.

- Typical mistakes made when creating a plan include: lack of a system and emergency savings, aimless investments, or planning only for a period of no more than 2-3 years.

Personal finance management is an important aspect of life that affects our financial well-being. To learn more about effective methods for managing your finances, it's worth exploring various sources of information. Start by reading specialized literature and articles on financial planning, investing, and saving. There are many online courses, webinars, and podcasts available online that will help you better understand the basic principles of financial literacy. It's also helpful to follow economic and personal finance news to stay informed about current trends. Don't forget about consulting with financial advisors who can offer personalized recommendations. By developing your knowledge in this area, you will be able to manage your finances more effectively and achieve your goals.

- If the phrase "saving money" conjures up unpleasant memories, read this article. In it, a financial development expert explains how to save more easily.

- To achieve your financial goals, you need not only to manage your income wisely but also to save money regularly. In this article, we've described 15 different ways to save the required amount.

- Once you've learned to rationally manage your budget and save for your goals, it's time to think about how to increase your capital. Various investment instruments can help. Read articles about stocks, OFZs, and a comprehensive investment guide for beginners.

- Those who want to effectively manage their personal finances may benefit from the Skillbox course "Personal Finance: Investments and Trading." It teaches you how to make plans, analyze the market, hedge against risks, and make a profit even in times of crisis.

Learn more about finance and investing with Skillbox Media materials. We offer relevant articles, helpful tips, and analytical reviews to help you understand complex financial issues and make informed investment decisions. Our content is designed to provide you with the knowledge and tools you need to successfully manage your finances and investments. Dive into the world of finance with Skillbox Media and develop your investing skills.

- Personal financial strategy: what is it and how to create it

- Financial literacy: what is it and how to improve it in adulthood

- 8 most common financial mistakes married people make

- Investing for beginners: where to start and what to study to get a stable income

- Is it worth investing in Russian stocks in 2025?

Personal Finance: Investing and Trading

Understand how to allocate a budget for investments and trade securities profitably. Learn how to make money and not lose money on investments. Begin your journey to financial freedom. The course speaker is Yulia Afanasyeva, a stock market investor with a personal trading account of over $1 million.

Find out more