Contents:

Free test: which digital profession is right for you? Find out the answer in 15 minutes and try your hand at a new Specialties.

Learn moreWhat is a family or joint budget?A family budget is a system for tracking the income received by all family members, as well as planning expenses and savings. Proper management of joint finances allows you to effectively allocate funds, control costs, and achieve financial goals. Creating and maintaining a family budget contributes to improved financial stability and helps avoid debt obligations.

Budget management is a key aspect of financial stability. It contributes to the achievement of goals, strengthens trusting relationships, and allows you to make reliable plans for the future. Effective budgeting also helps you prepare for unexpected financial situations, such as medical expenses, job loss, or equipment breakdown. Proper planning of financial resources provides confidence and protection in difficult situations.

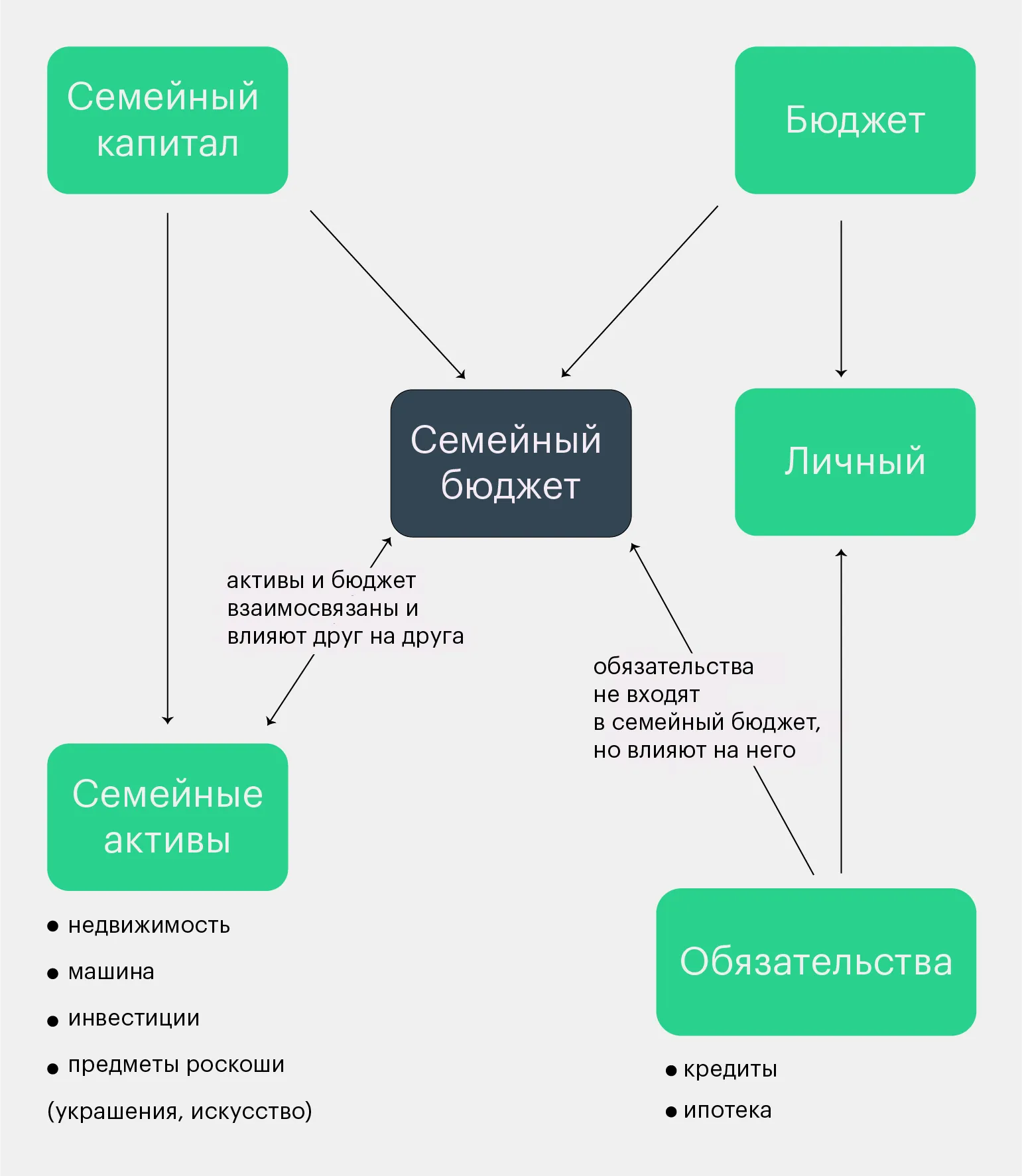

To effectively draw up a family budget, you need to understand its structure and the factors influencing it. The family budget is an important component of family capital. In addition to the budget, family capital includes assets that can generate income. These assets include real estate, cars, investments, jewelry, and interest-bearing bank deposits. Proper management of the family budget and assets will help ensure financial stability and achieve long-term goals. Budgets and assets are closely interrelated and influence each other. Effective budget management allows for the optimization of asset use, while the presence of stable assets facilitates more accurate budget planning. It is important to consider that changes in one of these areas can have consequences in the other. For example, increasing asset investments may require a revision of budget expenditures, while a lack of funding may limit the possibility of acquiring new assets. Thus, to achieve financial stability and growth, it is necessary to carefully analyze the interaction of the budget and assets, and develop strategies that take into account their mutual influence.

- Assets can generate a significant portion of income: an apartment can be rented out, and a car can be used as a taxi or courier.

- With the help of proper budget planning, you can replenish assets (buy shares or save up for a house).

When analyzing real estate and cars that are used as collateral for a loan, it is important to consider their financial performance. If loan payments equal or exceed the income received from these assets, they cannot be considered profitable investments. In this case, such properties do not generate income and can be considered liabilities. Properly assessing assets and liabilities will help you better manage your financial situation and make informed decisions.

Joint financial obligations, such as a mortgage, as well as the individual budgets of each partner, have a significant impact on the family budget. Personal financial obligations, including payments on loans for smartphones or alimony, also play an important role in the formation of the joint family budget. Effective management of these aspects will optimize expenses and improve the financial situation of the family.

To effectively analyze income and expenses, as well as to create a joint budget, it is necessary to consider all components of this financial system. Carefully accounting for all income, fixed and variable expenses will allow you to create a realistic and balanced budget that meets the needs of everyone involved. Analyzing cash flows will help identify weaknesses and optimize expenses, which will ultimately lead to increased financial stability.

To achieve effective SEO-optimized text, it is important to consider the keywords and phrases that users may enter in search engines. Here's an improved version of your text.

—

Reading is an important aspect of self-development and acquiring new knowledge. It helps broaden your horizons, improve critical thinking skills, and enrich your vocabulary. Regularly reading books, articles, and other materials contributes not only to personal growth but also to professional development. By devoting time to reading, you invest in your future, opening up new opportunities and horizons. Don't forget the importance of quality content: choose materials that are truly interesting and useful to you.

Read also:

Learning to save money is an important skill that will help you achieve financial independence and confidence in the future. The first step to effective savings is budgeting. Determine your income and expenses, highlight fixed and variable items to understand where your money goes.

Creating a financial safety net is another key aspect. It is recommended to set aside at least 10% of your income for emergencies. Automating your savings through banking services will make it easy for you to put money aside in a separate account.

A smart approach to spending also plays an important role in saving. Analyze your purchases and try to avoid impulsive spending. Plan large purchases in advance and look for alternative ways to save.

Investing is the next step to increasing your savings. Explore different investment vehicles, such as stocks, bonds, or real estate, to make the most of your savings.

By following these recommendations, you can not only learn how to save money but also create a stable financial base for your future goals.

Types of Financial Relationships in a Couple

People have different approaches to financial relationships, and the best option is one that is agreed upon by all participants in the couple. However, experts identify four main types of financial scenarios that help better understand how couples manage their money.

Breadwinner is a term describing a situation in which one partner provides all or a large part of the financial needs of a family or couple. This can occur in cases where only one partner is employed, or when one earns significantly more than the other. Such scenarios can impact relationship dynamics and the distribution of roles within the family. Understanding this situation is important for harmonious interaction between partners and for resolving issues related to finances and family responsibilities.

This model is especially relevant in situations where a woman goes on maternity leave. The key is to create a comfortable environment for all participants.

The breadwinner should remember that their financial situation does not give them the right to manipulate their partner. It is important for the partner with less income or no income to realize that their opinion and voice carry equal weight with those of the more financially successful partner. It is important to build relationships on mutual respect and equality, regardless of each partner's financial contribution.

"Sharing the pot" is an approach in which both partners pool all their earnings into a common account. These funds can be used regardless of the proportions of their contributions. This method allows for more effective financial management by creating a shared financial base for achieving joint goals.

Half-and-half is a concept in which each partner contributes half of their income to a common fund. Each person can use the remaining funds as they see fit. This model allows for the creation of a common good while ensuring financial independence for each participant. This practice can be useful for joint projects or collective initiatives where an equal distribution of resources and responsibility for their use are important.

Shared participation in the family budget is an approach in which partners determine what portion of their income each will contribute to shared financial expenses and what exactly they will be responsible for. For example, a husband can cover housing costs, loans, and travel, while the wife buys groceries and pays for children's extracurricular activities. This method of financial management helps avoid conflicts and promotes a more harmonious division of responsibilities within the family. Sharing money allows each family member to feel important and responsible, which ultimately strengthens financial stability and trust in the relationship.

How to Talk About Money

Managing a family budget starts with an open conversation. Before you start planning, it's important to discuss financial matters with your partner. Ask yourself a few key questions and encourage your partner to do the same. This will help you understand each other's financial goals, priorities, and expectations. Communicating about money creates the foundation for effective budget management and achieving financial well-being together.

- What is your current financial relationship as a couple?

- Are you happy with it? If not, why not?

- Do you have disagreements about money? If so, how do they manifest themselves?

- Have you discussed money matters before? If not, what stopped you?

- What feelings do you experience when you think about discussing financial issues?

How to talk

When each of you achieves clarity in understanding the management of the family budget, Discuss your views and ideas. Exchanging opinions will help you form a joint vision of financial management and strengthen the financial stability of your family.

- Clarify your position and needs. Talk with your partner about what money means to you and what place it occupies in your life, what level of income you want to have now and in the future.

- Talk about your partner's position. Listen carefully and clarify anything that is not clear. Consider the extent to which your views on financial matters coincide.

- Discuss a comfortable scenario for financial relations. Moreover, it is important to discuss the model that you see now and the one you strive for. And remember that financial relations can change over time. This is normal. The main thing here is to be honest with your partner.

- Train emotional intelligence. Resentments and disagreements may surface during the discussion. This is something that can and should be worked on if you aim to build relationships with each other and form common plans. Monitor the feelings you experience. Conversations about money require restraint and rationality. If you realize you or your partner are overwhelmed by emotions, it's best to talk later and reflect on the feelings that have arisen. Use the "I" position and consider what's behind your feelings.

- Work with anxiety. When it comes to financial matters, there are always things that worry you. Discuss triggers with your partner and come to a solution together.

Read also:

Emotional intelligence is the ability to recognize, understand, and manage one's own emotions, as well as the emotions of others. It plays a key role in interpersonal relationships, social adaptation, and professional performance. Developing emotional intelligence involves several aspects. First, it's important to learn to recognize one's emotions and understand how they influence behavior and decisions. Second, it's essential to develop empathy to better understand the feelings of others. Practicing communication skills and active listening also helps improve emotional intelligence. Practicing self-regulation, for example through meditation or reflection, helps control emotional reactions. Regular exercise and training in this area make a person more resilient to stress and improve their quality of life. By developing emotional intelligence, you not only become more empathetic to yourself and others, but also open up new opportunities for personal growth and career success.

How not to

Don't hide your income from your partner. Deception and omissions are unacceptable in relationships. Honesty is the foundation of successful and trusting relationships, and it should be demonstrated in all aspects, including financial matters. Openly discussing income helps build mutual understanding and trust, which is a key element of a healthy relationship.

A consulting psychologist and speaker of the course "The Art of Being Together" offers unique knowledge and practices aimed at developing partnerships. This course covers key aspects of interaction between partners, including effective communication, conflict resolution, and building trust. Participants will gain valuable tools for improving their relationships, helping them create a harmonious and happy life together. Join the course and learn the art of being together to make your relationship stronger and more fulfilling. If you have hidden financial sources and this becomes known, it can lead to serious conflict based on mistrust and underestimation of your partner. Money plays a key role in ensuring security in a relationship. When you share a household and suddenly discover secret expenses or income that do not contribute to improving the family's financial situation, this inevitably causes a feeling of anxiety and helplessness in your partner. Such situations undermine trust and harmony in relationships, making them important to discuss and manage together. Money is an area of transparency and trust. Dealing with finances requires clarity and understanding. An effective money management plan includes clear resource allocation, tracking of expenses, and careful budgeting. This approach not only simplifies financial transactions but also promotes a more conscious use of funds. Proper cash flow management allows you to avoid unnecessary expenses and accumulate funds for future investments.

- We talk about money openly and don't hide anything. Everyone knows everything.

- Each of us has pocket money, and no one reports on how it's spent. Each of us knows about our partner's money, but isn't interested in it.

- Each of us puts an equal percentage of our salary into a joint account (preferably a percentage rather than a fixed amount, because income can vary). This money is shared. Partners take from it as much as they need. They are accountable; we say what we spent it on."

Stay within the framework of discussing financial issues. It is important to maintain a dialogue and openly discuss emerging issues. Constructive conflict resolution requires the ability to accept criticism, justify your point of view, and avoid resorting to personal attacks. This approach promotes more effective interaction and strengthens trust in financial relationships.

Follow the agreed-upon terms. If you've established a shared budget, defined mutual goals, and developed a plan to promote saving and accumulation, it's important to strictly adhere to it. Avoid actions that could conflict with your partner's interests to maintain trust and harmony in the relationship. Don't manipulate the relationship. If you earn more, this doesn't give you the right to criticize or belittle a partner who earns less or is temporarily unemployed. Everyone has the right to participate in planning the family budget. It's important to consider each other's opinions and financial capabilities to create a harmonious and mutually beneficial relationship. Respect and understanding when it comes to finances will help strengthen your relationship.

Reading is an important aspect of personal and professional development. It helps broaden your horizons, improve communication skills, and increase your knowledge in various fields. Regularly reading books, articles, and other materials promotes critical thinking and creativity. In addition, reading can be an excellent way to relax and relieve stress. Remember to pay attention to the quality of the content you read, choosing sources that can bring you real benefits and new ideas.

Manipulation by loved ones, the media, and advertising is a common phenomenon that has a significant impact on our perceptions and behavior. Loved ones can use emotional tactics to achieve their goals, which sometimes leads to psychological pressure. The media, in turn, shapes public opinion and creates certain stereotypes, presenting information in a favorable light. Advertising actively uses manipulative techniques to encourage us to buy goods and services, causing us to feel compelled or afraid of missing out on something important. Understanding these mechanisms will help us become more critical of the information we receive and make conscious decisions.

How to manage a budget when you just moved in together

After discussing financial views and choosing a financial model that is convenient for both parties, you can move on to calculations. At this stage, it's important to consider all aspects, including income, expenses, and potential risks. Careful calculations will help avoid misunderstandings and ensure financial stability. Ensure all data is current and reflects the current financial situation. This will allow you to create transparent and effective financial plans that support the achievement of shared goals.

- Understand your budget after subtracting joint and individual obligations and each person's personal budget.

- Discuss regular shared expenses—rent, utilities, food. Will this all fall under the shared budget? Or will you divide these responsibilities and include them in your individual budgets?

- Discuss overspending—dining, events, medical expenses, and repairs. It's easiest to do this in a spreadsheet with expenses broken down into major categories. Perhaps you will feel more comfortable creating two joint budgets: one for regular expenses, and one for entertainment or something urgent.

CEO of the Financial Health service, expert of the course Financial Literacy: How to Set Financial Goals and Achieve Them. As part of the course, participants will learn how to effectively set financial goals and develop strategies for achieving them. We provide practical tools and techniques to help improve your financial situation and increase your financial literacy. Join us to master key personal finance skills and achieve your desired results. Keep the future in mind. If you're pursuing a serious, long-term relationship, it's important to consider shared goals and be prepared for financial commitments. One common mistake young couples make is neglecting savings and planning for the future. Marriage typically begins when partners are actively pursuing careers and increasing their incomes. However, as income increases, so do expenses. It's crucial to be mindful of your financial behavior and avoid overconsumption. Understanding and managing your finances will help you create a stable foundation for your future together.

Reworked text:

Also learn:

Financial literacy is the ability to effectively manage your finances, including budgeting, wise use of credit, and investing. Improving financial literacy in adults plays a key role in achieving financial independence and stability.

To begin with, it is useful to familiarize yourself with the basics of financial planning. This includes creating a budget, which will help you control your income and expenses. It is also important to understand how loans, interest rates, and loan terms work to avoid debt.

Reading specialized literature and participating in online courses on personal finance are excellent ways to increase your knowledge. It is also important to follow current trends in the financial world to make informed decisions.

Discussing financial issues with experienced professionals or participating in seminars can provide valuable insights and practical advice. Using financial apps will help you track your expenses and plan your budget more effectively.

Thus, financial literacy is not just a set of knowledge, but an important skill that requires constant updating and practice.

How to set joint goals and save money

In the course "The Art of Being Together." In "A Large Practical Course on Partnerships," financier and psychologist Natalia Stepanova offers helpful recommendations for improving partnerships. She shares effective methods and strategies that will help strengthen the bond between partners and create a harmonious atmosphere in the relationship. Natalia emphasizes the importance of communication, trust, and mutual understanding in couples, as well as how to effectively resolve conflicts and set shared goals. Participants will receive practical tools for developing emotional intimacy and improving the quality of their life together.

- Get specific with your goals. If your goal sounds like "we want to have enough for everything," that's the wrong goal setting. It's too abstract a concept and won't lead anywhere.

- Think about what kind of life you'd like to have in a year, three, or five years. What are the most important tasks you'd like to accomplish during this period? Perhaps this would be buying real estate or moving to another country.

- Look into the longer term. For example, you might need money for your child's education or for your retirement.

To achieve both long-term and short-term goals, it's important to digitize them. Write them down on paper or in an electronic document to clearly see the direction your family is heading. This will help you better organize your plans and track your progress.

According to the table, to achieve all your goals, you need to set aside 149,171 rubles every month. Your task is to assess how much this amount matches your budget. Consider ways to increase your income or optimize your expenses to successfully achieve this financial goal.

Discussing finances with your family is an important aspect that shouldn't be ignored. Conversations about income and goals should happen not only at the beginning, but also regularly. Establish a tradition with your partner to meet monthly to discuss financial plans and review progress. It's important to support each other if difficulties arise. At this stage, financial relations are not much different from what they were at the beginning of your marriage, but the level of responsibility and commitment increases. Regular discussions will help not only establish financial harmony but also strengthen trust in the relationship.

If you managed to create a transparent system for tracking family finances at the beginning, this will significantly simplify the process of planning family goals. Proper accounting will help you identify financial opportunities and set priorities, making achieving your goals more accessible.

Read also:

- Impulsive purchases - how to avoid them?

- 7 books on financial literacy

- How to improve relationships with your partner? Advice from psychologists