Contents:

Profession Accountant: Free access to course in 30 days

Find out moreWhat is a trial balance sheet (TBS) and its importance in accounting

A trial balance sheet (TBS) is an important accounting tool, generated in the form of a table. It shows the balances on the accounts of the Belarusian Standard Chart of Accounts at the beginning and end of the reporting period, as well as the company's turnover on debit and credit.

The main terms and principles of accounting in Belarus are regulated by the Law of the Republic of Belarus «On Accounting and Reporting» and regulatory acts of the Ministry of Finance of the Republic of Belarus (Ministry of Finance of the Republic of Belarus).

The balance sheet can be compiled for all accounts or for individual accounting accounts. In most cases, the statement includes key accounting items, such as:

- assets

- liabilities

- equity

- revenue

- Expenses,

- Profits and losses.

Companies independently determine the period for forming the balance sheet in accordance with their accounting policy, which is usually a month, quarter or year.

The main function of the trial balance sheet is to identify errors in accounting. The key objectives of forming the Balance Sheet are as follows:

- Checking the mathematical accuracy of entries in the accounting system - the total amounts of debit and credit should be equal (the principle of double entry).

- Confirming the correctness of the reflection of balances - credit balances should be on passive accounts, and debit balances on active accounts (in accordance with the Belarusian Standard Chart of Accounts).

Data from the Balance Sheet is used to prepare and verify the balance sheet and profit and loss statement in accordance with Belarusian standards.

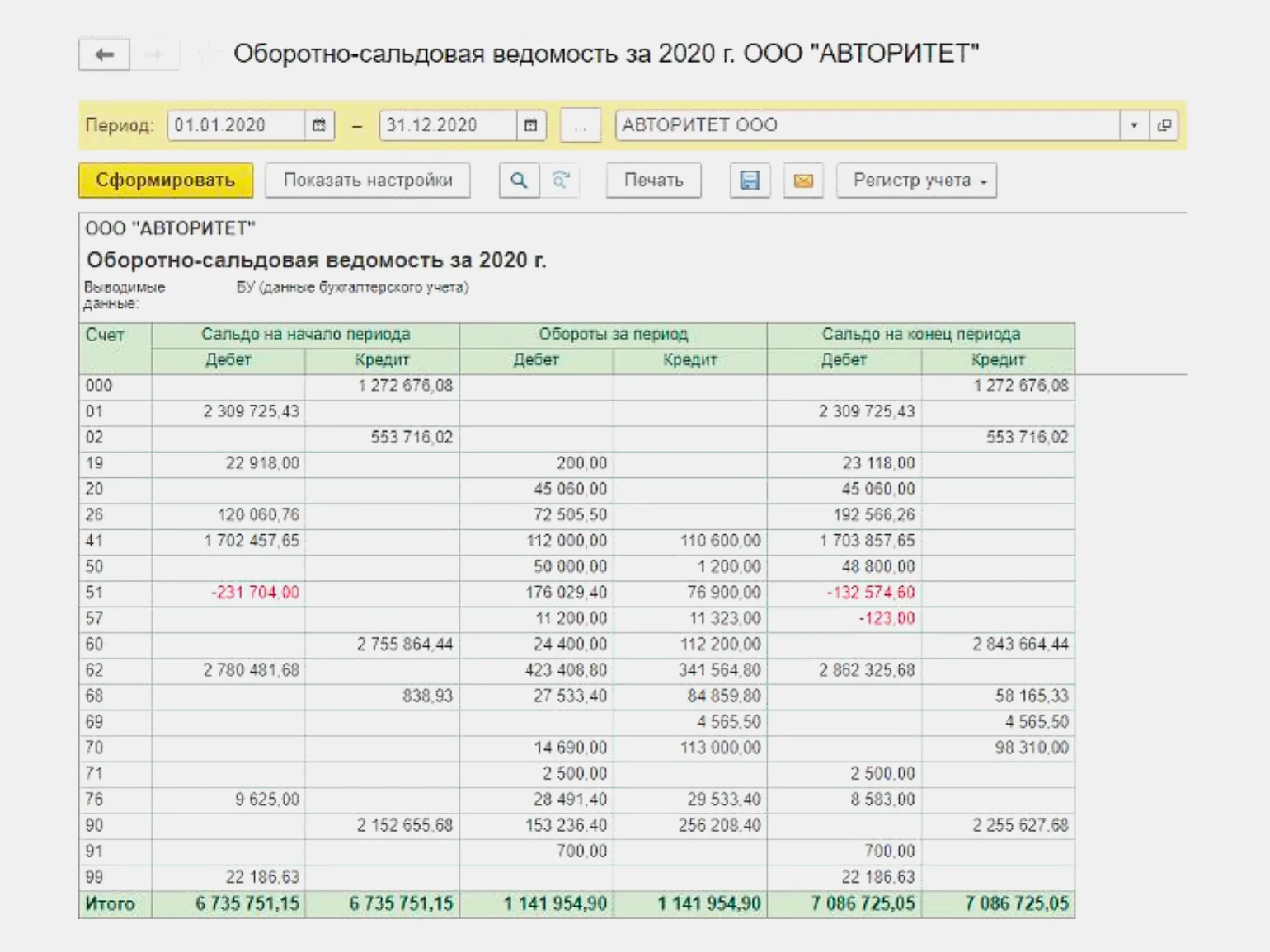

Below is an example of a balance sheet for Avtoritet LLC for 2020, generated automatically in the 1C: Accounting program.

It is important to note that submitting the final tax return to the tax authorities (the Inspectorate of the Ministry of Taxes and Duties of the Republic of Belarus - IMTS RB) on a regular basis is not required. However, the tax service may request this data during desk or on-site audits. The storage of trial balance sheets, like all primary documentation, is required for the periods established by the legislation of the Republic of Belarus (as a rule, at least 5 years, but there may be longer periods for certain documents).

The structure of the trial balance sheet (TBS): main elements

The trial balance sheet (TBS) is an important accounting tool, but there is no single generally accepted form for this document. Each company develops its own format, which is then approved in the appendix to the company's accounting policy.

As a rule, the OSV form may include the following elements:

- Lines reflecting the account numbers of the Belarusian Standard Chart of Accounts,for which financial transactions were carried out in a given period.

- Columns containing data on the "Balance at the beginning of the period", "Turnover for the period" and "Balance at the end of the period" indicating the balances on the debit and credit.

In addition, it should be taken into account that the T&C must include the following mandatory elements:

- Document title — “Turnover balance sheet”.

- Name of the company that compiled the T&C.

- Period for which the statement was compiled — month, quarter, year.

- The monetary value of accounting objects and the unit of measurement, for example, “thousand. rubles."

- The title of the specialist responsible for maintaining the balance sheet, for example, "accountant".

- The signature of the specialist responsible with his full name.

A Complete Guide to Preparing a Trial Balance Sheet

The trial balance sheet (TBS) is an important accounting tool that shows the state of accounts on a specific date. In modern conditions, the formation of the OSV is almost always performed automatically using specialized software adapted to the legislation of the Republic of Belarus.

Automatic formation (recommended method):

In Belarusian accounting systems, such as "1C: Accounting for Belarus", "Info-Accountant" or others, the process of creating the OSV is standardized:

- Go to the "Reports" section (or similar).

- Select the "Trial Balance Sheet" report.

- Specify the desired period for the report.

- Determine the level of detail of the information (by accounts, sub-accounts, analytics).

- Click the "Generate" ("Build") button.

The system will automatically create the balance sheet based on the entered transactions corresponding to the Belarusian chart of accounts.

Manual generation (theoretically possible, but extremely rarely used in practice):

- Transfer data from the "Balance at the end of the period" columns of the statement for the previous period to the "Balance at the beginning of the period" columns of the current balance sheet.

- Collect information on debit and credit turnovers for all accounts for the period from the accounting registers (Journals-Orders, Statements) and enter them in the "Turnover for the period" columns.

- Calculate the balance on all accounts at the end of the period using the formulas and enter this data in the "Balance at the end of the period" columns.

Checking the correctness of the balance sheet:

After generating the balance sheet (especially with the manual method), be sure to check its accuracy:

- Equal totals: the sum of debit balances at the beginning of the period must equal the sum of credit balances at the beginning of the period. The same applies to turnover for the period and balances at the end of the period. This is the main control point.

- Absence of negative balances: check for negative values where they are not allowed (for example, in cash and materials accounts).

- Account compliance: make sure that the balances of active accounts are debit, passive accounts are credit, and active-passive accounts are in accordance with their characteristics.

- Reconciliation with registers: check the totals of the general ledger account against the General Ledger data or journals and orders.

The OSV can be issued in either paper or electronic form. The employee who prepared it (usually the accountant or chief accountant) signs the paper copy. In electronic form, it is generated and stored in the accounting program database.

For a deeper understanding of accounting and reporting in Belarus, we recommend that you familiarize yourself with the materials on the official websites:

- Ministry of Finance of the Republic of Belarus (MBF): https://www.minfin.gov.by/

- Inspectorate of the Ministry of Taxes and Duties of the Republic of Belarus (IMTS RB): https://www.nalog.gov.by/

- National Legal Internet Portal of the Republic of Belarus (pravo.by): https://pravo.by/ (to search for laws and regulations).

Why do you need a trial balance sheet?

- Control: ensures continuous monitoring of the company's assets, liabilities, capital, income and expenses.

- Error detection: the main tool for checking the correctness of the posting of transactions to accounts and compliance with the double-entry principle. Equality of results is an indicator of arithmetic correctness.

- Reporting basis: a direct source of data for filling out the annual and interim financial statements of Belarus.

- Analysis: allows for financial analysis, assessment of liquidity, profitability, and capital structure.

- Audit: is the main document for conducting both internal and external audits.

- Data confirmation: serves to verify data with other registers (General Ledger, order journals) and primary documents.

Frequently Asked Questions about the Trial Balance Sheet

- How often should the Trial Balance Sheet be prepared?

The Trial Balance Sheet is prepared at the end of each reporting period established by the organization's accounting policy. Most often - monthly (for internal needs, preparation of quarterly reports) and mandatory - at the end of the year (for the formation of annual financial statements). Quarterly consolidated financial statements are also common.

- What to do if there are errors in the consolidated financial statements?

Errors in the consolidated financial statements must be corrected immediately after their discovery.

First, find the source - an incorrect transaction, an arithmetic error in the primary document or register, an omitted transaction.

Errors are corrected in the month in which they are discovered. The methods provided for by the legislation of the Republic of Belarus are used: reversal entries (to cancel an erroneous transaction), additional entries (if the transaction is not reflected or is reflected in a smaller amount), corrective entries (in special cases). All corrections must be documented (for example, an accounting certificate). After corrections, the balance sheet is regenerated.

- Who signs the balance sheet?

The balance sheet is typically signed by the accountant who prepared it and/or the organization's chief accountant. This confirms responsibility for the accuracy of the data presented. The signature form (on paper or electronically) is determined by the accounting policy.

Accounting: 5 key skills for a successful career

Want to become an accountant from scratch? Learn 5 important skills for a successful career in our article!

Learn more