Contents:

- What are International Financial Reporting Standards (IFRS)?

- Comparison of IFRS and RAS: Key Differences

- Who is required to report under IFRS in Russia?

- Reporting Requirements under IFRS

- Reporting Requirements under IFRS

- Conclusion

- Key Principles of IFRS: Fundamentals of Financial Reporting

- Key Aspects of IFRS: 4 Main moment

Financial Manager: 7 Steps to a Successful Career

Learn MoreWhat are International Financial Reporting Standards (IFRS)?

International Financial Reporting Standards (IFRS), also known as IFRS (International Financial Reporting Standards) and IAS (International Accounting Standards), are a set of principles and standards that define the rules for preparing financial reports for companies. These standards help ensure uniformity and transparency of financial reporting at the global level, which is important for investors, creditors, and other stakeholders. The implementation of IFRS improves the comparability of financial data across organizations and countries, which contributes to more effective business decision-making. IFRS standards are constantly updated and adapted to changes in the financial environment, making them relevant and essential for modern businesses. Financial statements prepared in accordance with International Financial Reporting Standards (IFRS) include important indicators such as revenue, net profit, losses, operating results, and tax expense. These indicators are crucial for investors and creditors, as they allow them to assess a company's financial condition and make informed decisions about providing financing. Clearly presenting this data helps not only in analyzing the current situation but also in predicting the company's future performance, which is important for all stakeholders. Since their introduction in 2001, International Financial Reporting Standards (IFRS) and International Accounting Standards (IAS) have covered many aspects related to the preparation and presentation of financial statements. Companies operating internationally are required to comply with both IFRS and IAS, ensuring consistency and transparency in financial statements. For a complete list of standards and up-to-date information, visit the official website of the IFRS Foundation. Compliance with these standards is critical to ensuring investor and other stakeholder confidence in companies' financial information.

Today, more than 167 countries, including the United States, Australia, South Africa, China, and Russia, have implemented International Financial Reporting Standards (IFRS). This underscores the global recognition and importance of these standards in the international financial system. The use of IFRS contributes to increased transparency of financial statements and facilitates international cooperation in business and investment.

In Russia, International Financial Reporting Standards (IFRS) were officially implemented in 2010 with the adoption of Federal Law No. 208-FZ "On Consolidated Financial Statements." This law requires insurance companies, credit institutions, non-state pension funds, and other large enterprises to use IFRS in their financial statements. For more detailed information on IFRS, we recommend referring to specialized publications and resources dedicated to financial standards, where you can find up-to-date data and recommendations for their application.

Comparison of IFRS and RAS: Key Differences

International accounting uses International Financial Reporting Standards (IFRS), which differ significantly from Russian Accounting Standards (RAS). All companies registered in Russia are required to comply with RAS, with the exception of banks and credit institutions. Understanding the differences between IFRS and RAS is important for effective accounting and the preparation of financial statements that comply with the requirements of both national and international legislation. The use of IFRS allows companies operating in the international market to present their financial statements more transparently and reliably, which helps increase the confidence of investors and partners.

For an in-depth study of RAS, we recommend reading this article, which examines in detail the key aspects of this standard.

The main differences between IFRS and RAS can be analyzed by several key criteria. Firstly, IFRS (International Financial Reporting Standards) are focused on global markets and international companies, while RAS (Russian Accounting Standards) were developed taking into account the specifics of the domestic economy and legislation. Secondly, IFRS assume the application of the fair value principle, while RAS more often focus on the historical cost of assets. Thirdly, the preparation of financial statements under IFRS requires a greater degree of disclosure, which contributes to increased transparency for investors and creditors. It is also worth noting that IFRS places greater emphasis on the valuation of assets and liabilities, while RAS emphasizes the reliability of registration records. These differences affect the reporting methodology and the interpretation of financial indicators, which is important to consider when analyzing the financial position of organizations.

Reporting in accordance with Russian Accounting Standards (RAS) is focused on both the internal and external interests of users. It provides important data for analysis, allowing company executives, managers, tax authorities, and creditors to make informed decisions. Based on these reports, management can assess business expansion prospects, while tax authorities verify the accuracy of accounting records, which can prevent potential fines and sanctions. Accurate and timely reporting under Russian Accounting Standards (RAS) plays a key role in ensuring financial transparency and trust among all stakeholders. International reports prepared in accordance with International Financial Reporting Standards (IFRS) are aimed at external investors and business partners. These reports provide the necessary information for analyzing a company's financial condition and assist in making informed investment decisions. IFRS ensures transparency and comparability of financial data, allowing investors to more accurately assess the risks and opportunities associated with investing in a company. RAS establishes a mandatory requirement for the preparation of financial statements in rubles for a fixed reporting period from January 1 to December 31. This ensures consistency and transparency in accounting and reporting for all organizations operating under Russian standards.

IFRS allows the use of various currencies chosen by company management. This provides greater flexibility in financial reporting. In addition, companies have the ability to choose any reporting periods, which contributes to a more accurate reflection of the financial position and operating results.

When preparing reports in accordance with International Financial Reporting Standards (IFRS), the fair value of assets is assessed, while Russian Accounting Standards (RAS) are based on historical cost. For example, a plant acquired in the 1990s may be accounted for in RAS at a low historical cost. At the same time, under IFRS, its fair value may be significantly higher, reflecting real market conditions. This difference in approaches to asset valuation can have a significant impact on a company's financial results and performance, so it is important to take these aspects into account when preparing reports.

IFRS emphasizes the importance of the economic meaning of transactions, giving accountants the opportunity to apply professional judgment in selecting the appropriate accounting standard. In contrast, RAS emphasizes document flow and strict compliance of accounting records with submitted documents. This difference in accounting approaches reflects the different goals and objectives of financial reporting under international and Russian standards. The use of IFRS allows for more flexible accounting of financial transactions, while RAS requires strict adherence to established rules and procedures.

The differences between IFRS and RAS are significant. The choice between these accounting systems depends on the specifics of the business and financial reporting requirements. IFRS (International Financial Reporting Standards) offer a more universal and transparent approach to accounting, which may be important for companies operating in international markets. At the same time, RAS (Russian Accounting Standards) are better suited for companies focused on the domestic market, as they take into account the specifics of national legislation. Choosing the right accounting system not only optimizes financial processes but also increases the trust of investors and partners.

Who is required to maintain IFRS reporting in Russia?

According to Federal Law No. 208-FZ of July 27, 2010, "On Consolidated Financial Statements," a list of organizations required to comply with International Financial Reporting Standards (IFRS) in Russia has been established. These organizations occupy an important place in the country's financial system, ensuring the transparency and reliability of financial data. Compliance with IFRS improves the quality of financial information, which, in turn, helps increase the confidence of investors and creditors. English: It is important to note that the correct application of IFRS helps organizations not only comply with legal requirements, but also optimize their financial processes.

- credit institutions;

- insurance companies, with the exception of those that deal only with compulsory health insurance;

- non-state pension funds;

- management companies of investment funds, mutual investment funds and non-state pension funds;

- joint-stock companies whose shares are in federal ownership;

- clearing organizations;

- federal state unitary enterprises;

All companies whose securities are listed are required to prepare financial statements in accordance with International Financial Reporting Standards (IFRS). This requirement plays a key role in ensuring the transparency of financial data and increasing investor confidence. IFRS reporting allows investors to more accurately assess a company's financial condition, which facilitates more informed investment decisions.

Russian companies continue to face the requirement to prepare reports in accordance with International Financial Reporting Standards (IFRS), while also being required to maintain financial statements in accordance with Russian Accounting Standards (RAS). This dual requirement ensures compliance with both international and national regulations, which is important for businesses seeking transparency and trust from investors and partners. Adherence to both systems allows companies to effectively manage their finances and minimize the risks associated with non-compliance.

IFRS Reporting Requirements

According to the International Financial Reporting Standard IAS 1 "Presentation of Financial Statements," companies are required to prepare a complete set of financial statements. These statements play a key role in ensuring the transparency and comparability of financial information, which, in turn, facilitates a better understanding of the company's financial condition by stakeholders. Compliance with this standard helps organizations present their results effectively, improving the confidence of investors and other market participants.

- Statement of Financial Position - This document shows the current value of the company's assets, liabilities, and equity as of specified dates.

- Statement of Profit or Loss and Other Comprehensive Income - It presents information about the company's revenues and expenses for a selected period, which allows you to evaluate its financial performance.

- Statement of Changes in Equity - This statement shows how shareholders' equity has changed during the reporting period, including retained earnings or loss, as well as changes in the number and par value of shares.

- Statement of Cash Flows (CSFS) - This statement shows all cash receipts and payments during the reporting period, as well as cash balances at the beginning and end of that period.

Each of these statements must be accompanied by explanatory notes, including a brief description of the accounting policies. This allows users of the statements to better understand the principles on which the financial statements are based. This approach improves the transparency and trust in the information presented, providing a more complete understanding of the financial position and performance of the organization.

Requirements for reporting under IFRS

When preparing financial statements in accordance with IFRS (International Financial Reporting Standards), it is important to consider several key aspects. The main requirements include data comparability, materiality, and substance over form. Let us consider each of these aspects in more detail. Data comparability allows users to analyze financial information over different periods and between different organizations. Materiality implies that the information must be meaningful to users so that they can make informed decisions. The predominance of substance over form means that it is important to consider the actual economic substance of transactions, and not just their legal form. Following these principles helps ensure high-quality and transparent financial reporting.

Comparability of data in financial reporting plays a key role. Information presented in reports for different financial periods must be comparable to ensure accurate analysis. This helps identify trends and dynamics in indicators, which, in turn, facilitates informed decision-making. Comparing financial data helps investors, creditors, and other stakeholders evaluate business performance and its financial condition over time.

Data for both the current and previous years must be provided to clearly reflect changes. It is important to keep the calculation formulas constant for both periods, which will ensure the correctness of comparison and analysis.

If a company makes changes to its accounting policies and calculation formulas, it is obliged to restate the indicators for all previous periods in accordance with the new rules. This mandatory action ensures comparability of data and complies with the requirements of International Financial Reporting Standards (IFRS). Timely updating of calculations helps ensure the transparency and reliability of financial statements, which ultimately contributes to increased confidence from investors and other stakeholders.

In the context of financial reporting, materiality means that a company is required to disclose information about indicators that are significant to users of the reports. Information is considered material if its absence or misstatement could influence the decisions of users such as investors and creditors. Correct presentation of material information helps avoid misunderstandings and reduces risks for all stakeholders, ensuring transparency and trust in the company's financial data.

This requirement indicates that the information in the reports should reflect the economic substance of transactions, and not just their legal form. For example, if a company receives financing by pledging equipment as collateral, this should be reflected as a loan, not as income from the sale of assets. Therefore, it is important to adhere to the principle of economic substance to ensure the accuracy and reliability of financial statements. This helps report users better understand the company's true financial position and make more informed decisions.

Legally, a business may be considered a seller, but in practice, it represents borrowed funds. In accordance with International Financial Reporting Standards (IFRS), it is important to disclose the amount of the loan and the associated interest expense. This will more accurately reflect the company's true financial position and improve the transparency of its reporting for investors and creditors. Proper presentation of loans and interest expenses in reporting contributes to a clearer perception of financial risks and liabilities, which is a key factor in making informed business management decisions.

Conclusion

By adhering to these principles, companies can ensure the transparency and reliability of their financial reporting. This is critical for both internal analysis and interaction with external users. For a deeper understanding, we recommend visiting official resources such as IFRS.org and FASB.org, which provide up-to-date information and guidance on international financial reporting standards.

Key Principles of IFRS: The Basics of Financial Reporting

International Financial Reporting Standards (IFRS) establish the core principles that ensure the transparency and comparability of financial data globally. These standards play a key role in the preparation of financial statements, allowing users to accurately assess the financial condition and performance of companies. It is important to highlight two main principles that determine the structure of financial statements, which contributes to a clearer understanding and analysis of the data presented.

The accrual basis of accounting is fundamental to IFRS financial statements. All financial statements, with the exception of the statement of cash flows, are prepared taking into account this principle. This means that income and expenses are reflected in accounting records when they arise, and not when cash is actually received or paid. The accrual accounting principle allows for a more accurate reflection of a company's financial condition and operating results, which is especially important for analysis and forecasting. Therefore, adherence to this principle plays a key role in ensuring the transparency and reliability of financial information.

If a company has shipped goods, but the buyer has not yet paid for them, the income statement should include the sales revenue. This is necessary for a more accurate assessment of the company's financial position, as it reflects real business transactions, regardless of actual cash receipts. This approach helps provide a more objective picture of the financial statements and facilitates more informed management decisions.

If a company has used services but has not yet paid for them, these expenses should be included in the statements. This will reflect the real financial burden on the organization and provide an accurate picture of its financial position. Accounting for such liabilities is important for the correct analysis of cash flows and for assessing the overall performance of the business.

The going concern principle is key for companies, as it implies the organization's intention to continue its activities in the future, without the threat of bankruptcy. This is an important aspect, as it directly affects the valuation of the company's assets in the financial statements. Asset valuation based on this principle allows users of financial information to more accurately assess the financial condition and development prospects of the company. Thus, adhering to the going concern principle enhances the confidence of investors and other stakeholders.

If a company is in liquidation or anticipates bankruptcy, the liquidation value of assets should be used in reports prepared under International Financial Reporting Standards (IFRS) instead of their fair value. This change can significantly impact a company's financial performance. Liquidation value reflects the true value of assets in liquidation, which is important for stakeholders such as creditors and investors. Correct use of liquidation value helps ensure the transparency of financial reporting and allows for a more accurate assessment of the company's financial position in difficult situations.

For a deeper understanding of International Financial Reporting Standards (IFRS) and their practical application, we recommend studying the official documents posted on the IFRS Foundation website. These materials will help you better navigate the complexities of IFRS and ensure compliance with international requirements in financial reporting.

Incorrect application of the principles of International Financial Reporting Standards (IFRS) can lead to serious consequences for companies. Firstly, it can lead to distortion of financial statements, which makes it difficult to make informed business decisions both within the company and by investors. Secondly, non-compliance with the standards can lead to legal consequences, including fines and sanctions from regulatory authorities. Thirdly, it can negatively affect the company's reputation, which, in turn, will reduce the trust of partners and customers. It is important to ensure the correct application of IFRS to maintain financial transparency and increase the level of confidence in the organization's reporting.

Incorrect application of accounting principles can lead to distortion of financial statements. This, in turn, can negatively impact the confidence of investors and other stakeholders. Strict adherence to accounting principles is key to ensuring the transparency and reliability of financial reporting.

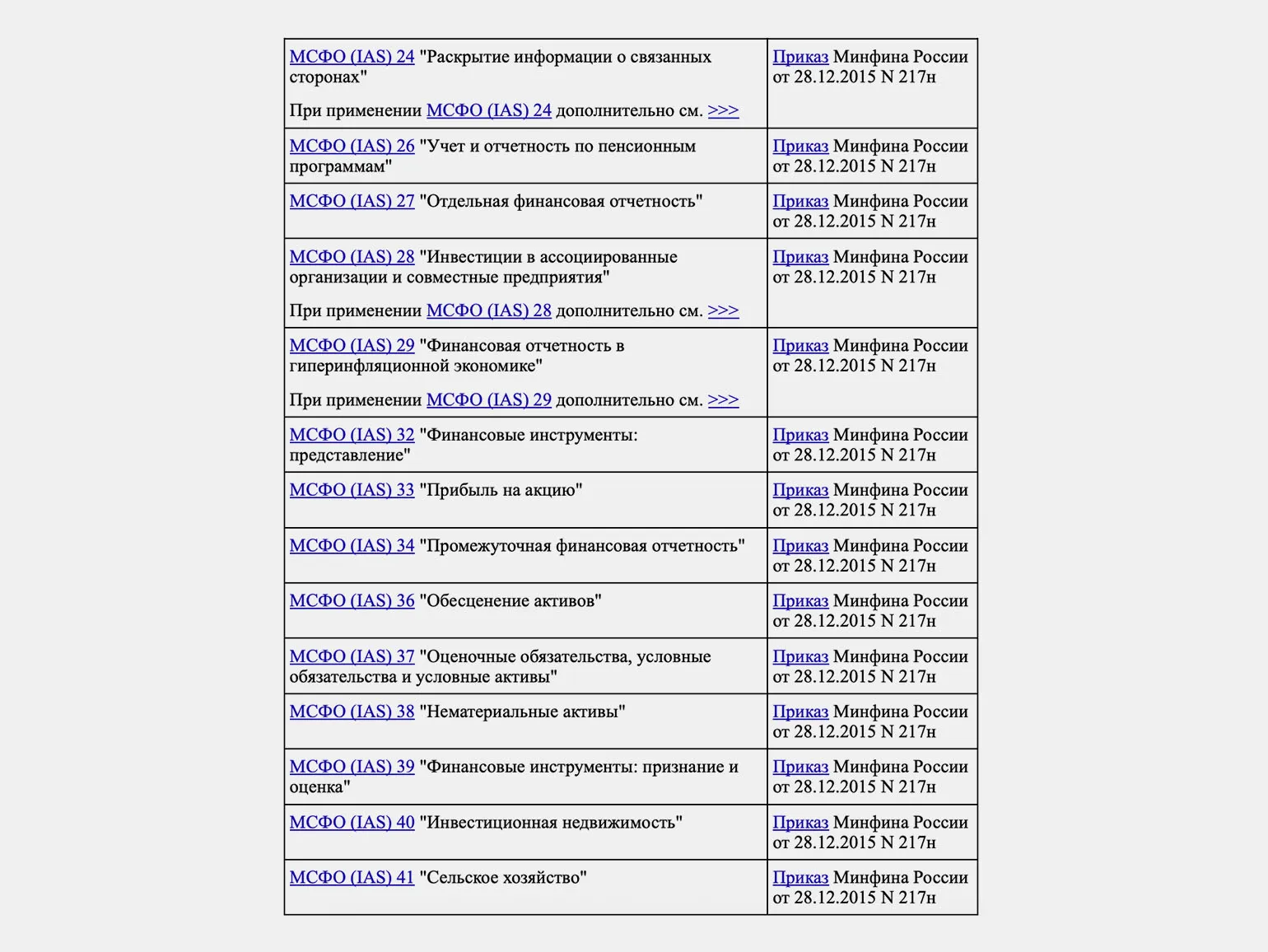

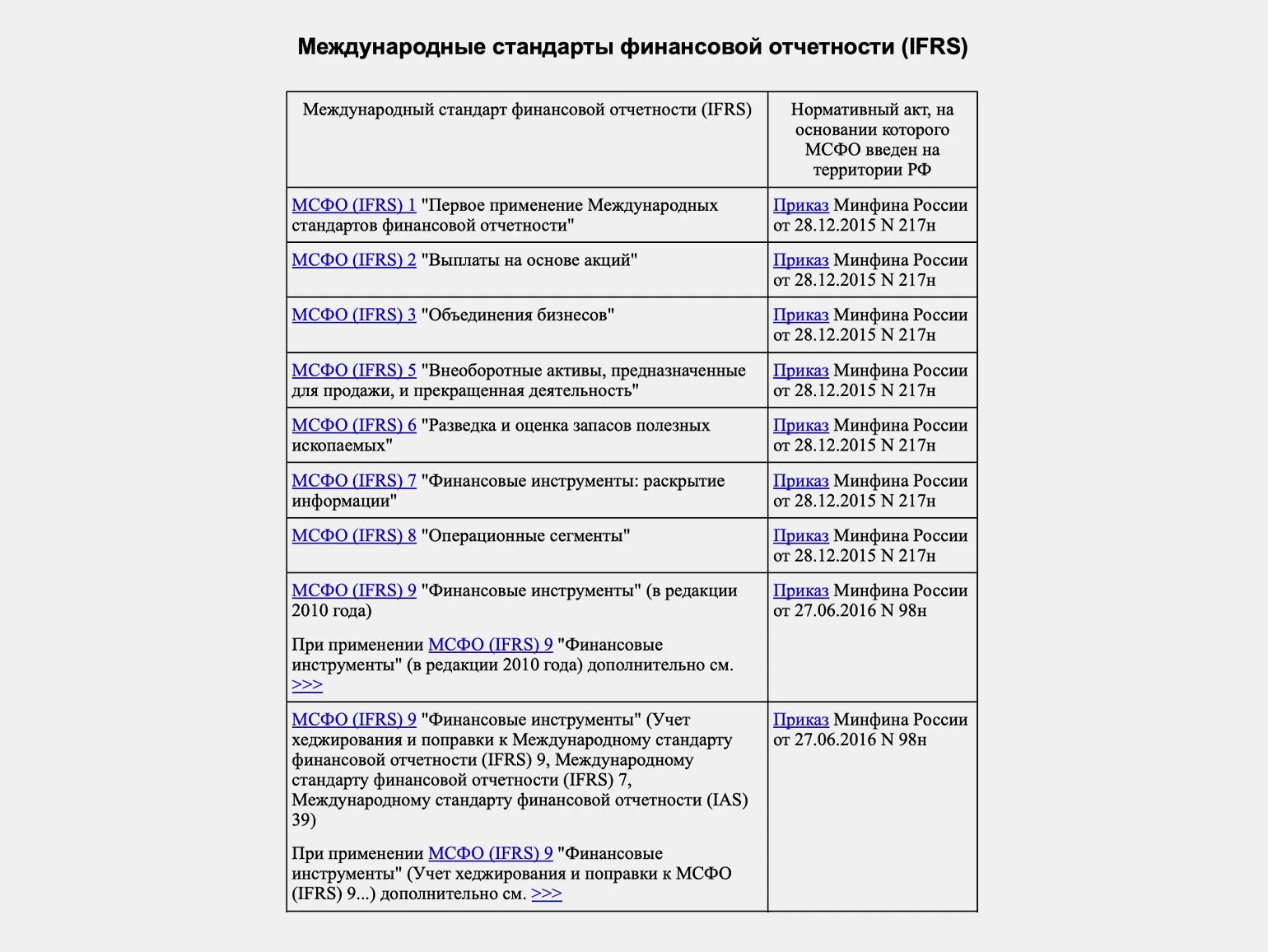

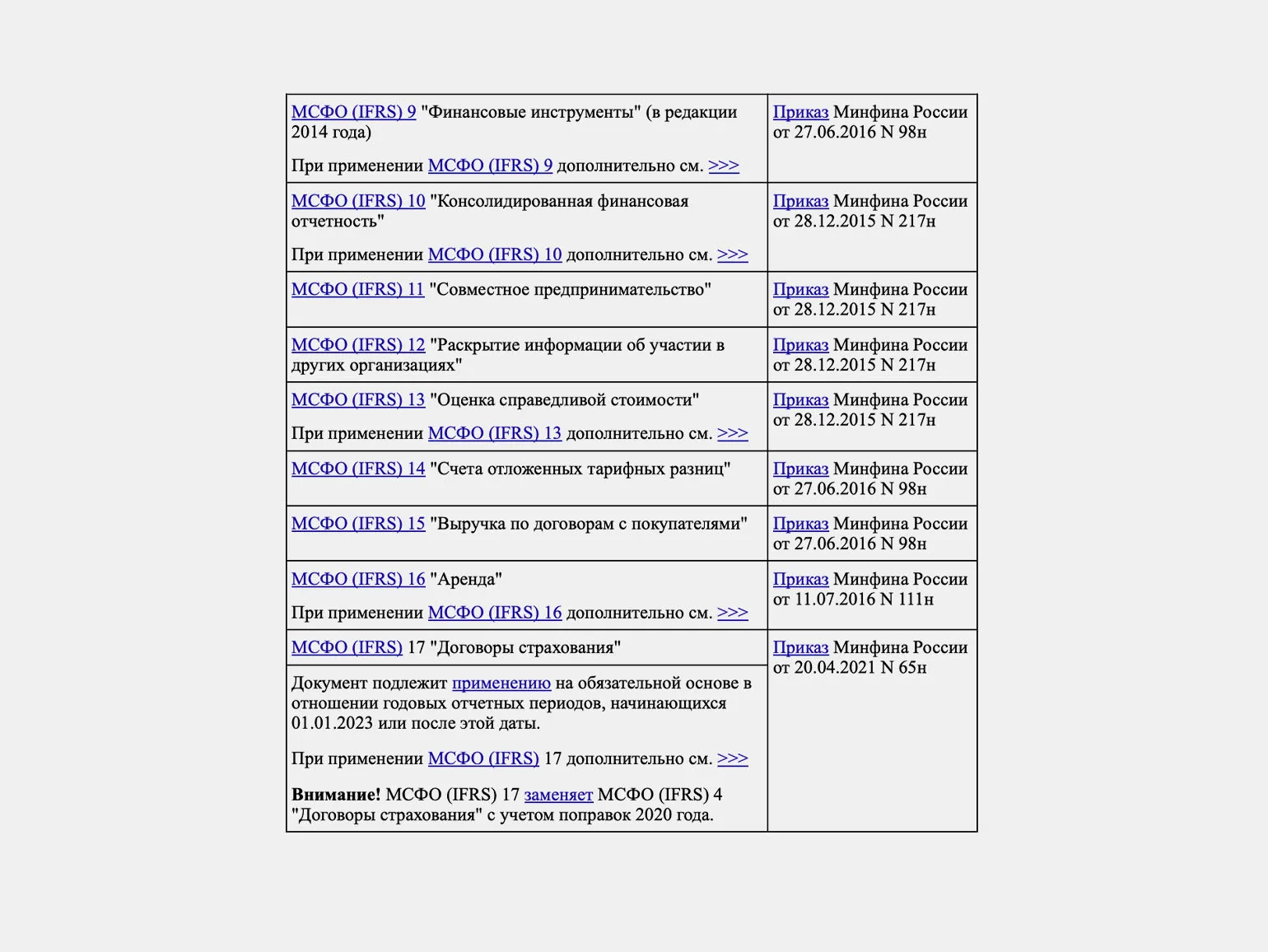

International Financial Reporting Standards (IFRS) are updated regularly. The updating process is carried out by the International Accounting Standards Board (IASB), which monitors changes in the financial environment and the needs of reporting users. Updates typically occur annually, but extraordinary changes may occur in response to important events or changes in legislation. It is important for companies to monitor the latest updates and adapt their financial statements to the new IFRS requirements to ensure transparency and reliability of information for investors and other stakeholders. Timely updating of standards helps improve the quality of financial reporting and increase trust in it in international markets.

International Financial Reporting Standards (IFRS) are regularly updated and revised. These changes are aimed at adapting to the changing economic environment and improving the quality of financial reporting. Updates to IFRS standards improve the transparency and comparability of financial data, which is important for investors and other stakeholders. Therefore, compliance with current IFRS standards helps companies increase the credibility of their financial statements and improve management decision-making.

Key Aspects of IFRS: 4 Key Points

- International Financial Reporting Standards (IFRS) are a set of principles and rules for the preparation of financial statements, ensuring their transparency and comparability globally.

- In the Russian Federation, the obligation to report in accordance with IFRS applies to nine categories of organizations, including banking institutions, insurance companies, clearing organizations, and mutual investment funds. Other companies may adopt IFRS on their own initiative, especially if they plan to enter international markets.

- It should be noted that compliance with IFRS does not exempt companies from the obligation to prepare financial statements in accordance with Russian Accounting Standards (RAS).

- When preparing reports in accordance with IFRS, it is necessary to take into account the requirements for the quality of reporting: data must be comparable, indicators must be material, and the results must be justified and economically justified. This requires companies to carefully analyze and prepare.

Financial Manager: 5 Steps to a Salary of 60,000 Rubles.

Do you want to become a financial manager with a high salary? Learn 5 key steps to a successful career!

Learn more